2018 SMSF Annual Return and Taxation

Section B: Income - Did you have a capital gains tax (CGT) event during the year?

The SMSF Annual Return has the updated text "If the total capital loss or total capital gain is greater than $10,000 or you elected to use the CGT relief in 2016/17 and the deferred notional gain has been realised, complete and attached a Capital gains tax (CGT) schedule 2018"

This will mean that it will be mandatory to produce the CGT Schedule if a deferred notional gain has been realised during the Financial Year even if the total capital loss or total capital gain is less than $10,000

Section B: Income - Changes to the Net Capital Gain Calculation for deferred notional gains

CGT relief was also provided for certain SMSFs in the 2016/17 income year. For the 2017/18 year where the SMSF has a deferred notional gain amount for an asset and that asset has been disposed of during the 2017/18 year, the SMSF will need to report that the deferred notional gain has been realised in the CGT Schedule.

This creates a change for the 'CGT method statement' and the Calculation of Net Capital Gains.

When this asset is sold which has a deferred notional gain amount, the deferred capital gain is recognised. This deferred gain will not be discounted in the realisation year, however it is to be reduced by capital losses made in that year as well as carried forward losses. Any exempt proportion e.g Actuarial Percentage applied for the realisation year e.g 2017/2018 does not apply to the deferred gain, as the relevant exempt proportion from the 2016–17 year was applied to this deferred gain.

Simple Fund 360 automatically calculates the correct Net Capital Gain Amount and will populate the Capital Gains Schedule correctly.

Section B: Income - Change to ECPI and Net Capital Gain Calculation

If the assets of an SMSF are segregated for only part of an income year and you wish to claim ECPI for the remaining period of the year in which the assets of your SMSF are unsegregated, you will be required to obtain an actuarial certificate for the period your fund's assets are unsegregated.

The previous approach by the ATO and the industry was to either apply the Segregated or Unsegregated method for the entire year. The interpretation for this legislation now means:

- In instances where all of an SMSF's assets are held 'solely' to meet super income stream benefit liabilities it has to pay, then 100% of the fund's assets are used to support pension liabilities and the position is that all of the fund's assets in these circumstances are classified as segregated current pension assets.

- This means that for any portion of any income year (i.e any part of the year) where an SMSF's assets are held solely to meet super income stream liability benefits (i.e. any period that the SMSF is in 100% pension phase) the SMSF trustee is required to calculate its ECPI for that portion of the income year using the segregated method. An actuarial certificate is not required to support the SMSF's calculation of ECPI for this period when all of the fund's assets are classified as segregated current pension assets.

- For any portion of an income year (i.e any part of the year) that an SMSF is not in 100% pension phase, for example, its members have a mix of pension phase and accumulation phase interests for part of the year, and the SMSF's assets are not segregated, the SMSF trustee will be required to use the proportionate method to determine its ECPI for that period. That is, the SMSF trustee will be required to obtain an actuarial certificate if they wish to claim ECPI in relation to income received by the fund during that part of the income year.

- The actuary will calculate the proportion of the fund’s assets that are supporting super income stream liabilities during that part of the year when the fund’s assets were not segregated. The SMSF trustee is then required to apply the proportion determined by the actuary to the income received by the fund during the relevant period as a component of the fund’s ECPI for the income year.

Example:

At 1st July, a fund has 2 members with one in pension mode and one accumulation mode. On 1 March the accumulation member converts from accumulation phase to pension phase making the fund 100% pension phase for the remainder of year

|

2017 and prior treatment

|

2018 FY Treatment

|

|---|---|

|

|

Simple Fund 360 automatically calculates the correct Net Capital Gain Amount and will populate the Capital Gains Schedule correctly based on the details on the Fund Pension Policies screen.

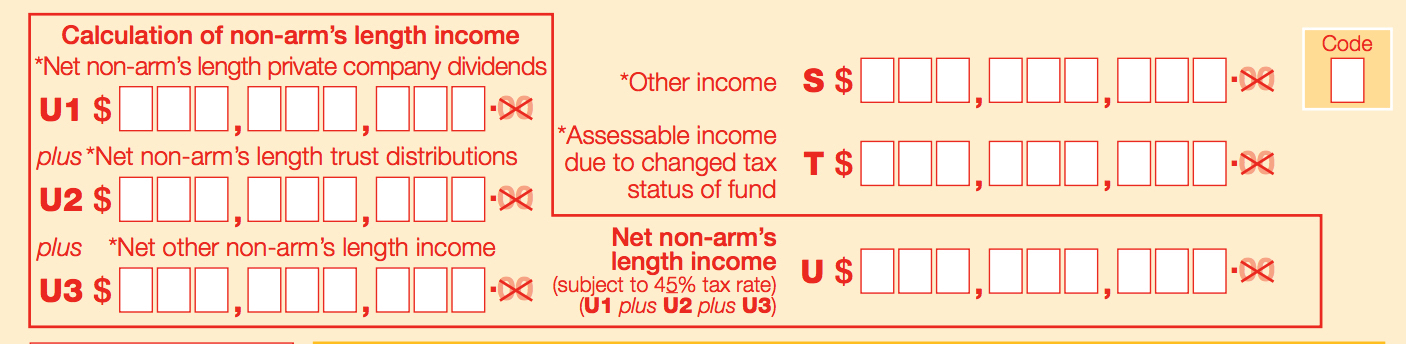

Section B: Income - Net non-arm’s length income

The tax rate for non-arm’s length income has changed from 47% to 45%

Various rates of tax that apply to superannuation entities have been decreased in line with the cessation of the temporary budget repair levy which was payable by some individuals from 2014–15 through to 2016–17.

Rates affected include those that apply to the taxable income of non-complying superannuation funds and the non-arm’s-length component of the taxable income of a superannuation fund.

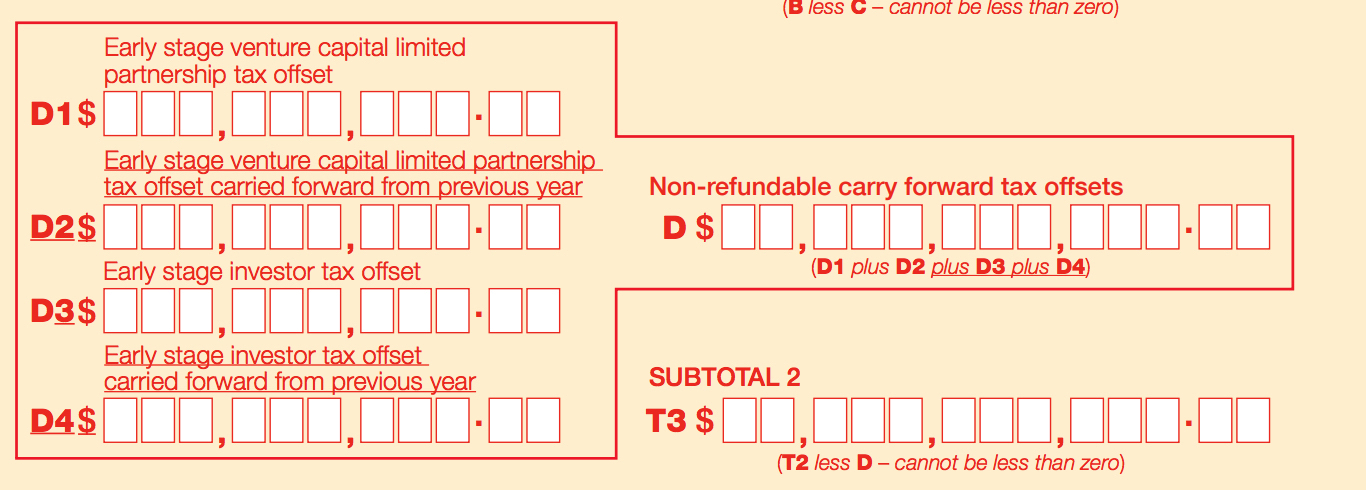

Section D: Income tax calculation statement - Non-refundable carry forward tax offsets

New labels have been added for 'Early stage venture capital limited partnership tax offset carried forward from previous year' and for 'Early stage investor tax offset carried forward from previous year'.

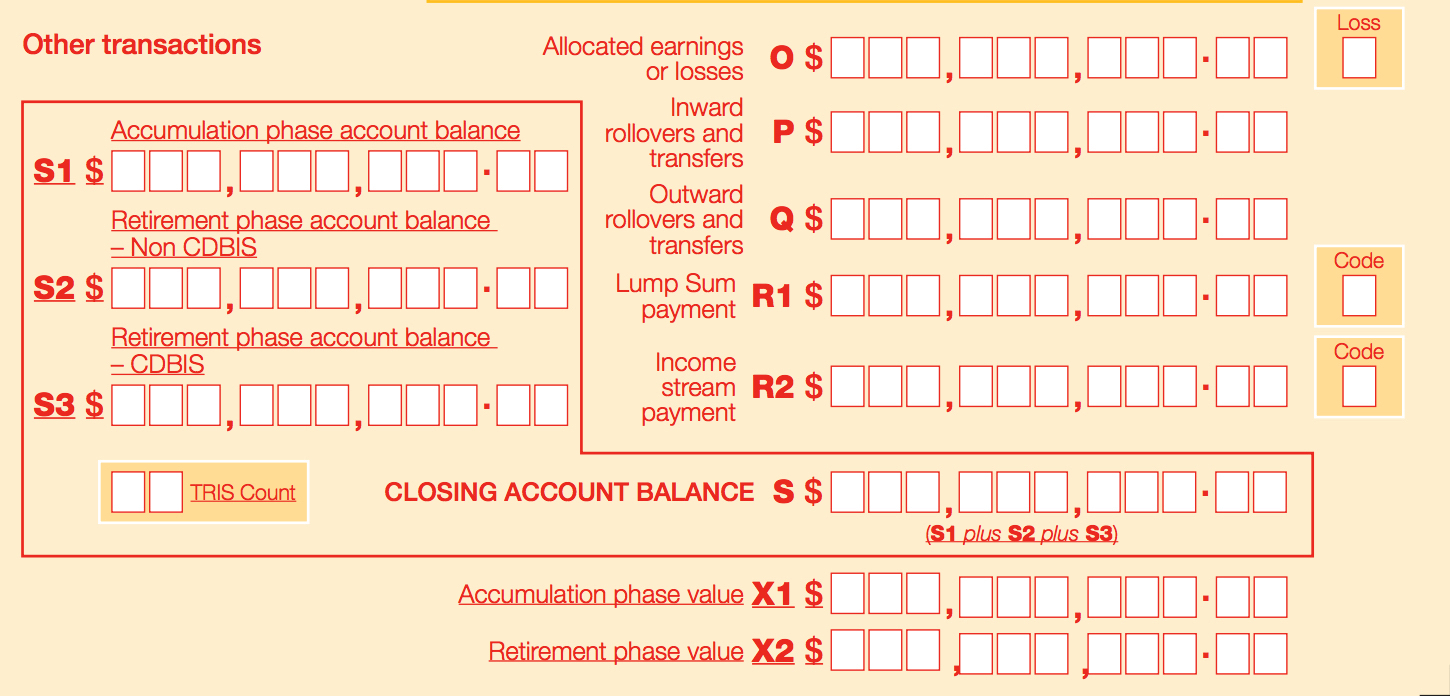

Section F&G: Members - Members Accumulation and Retirement-Phase Balances

Each member will now need to report what is their Accumulation phase balance and Retirement phase balance as at June 30.

The Superannuation Reforms contained multiple super changes that will be dependent on an individual’s Total Superannuation Balance (TSB) which will be a 30 June balance amount reported for each member.

The TSB will be used to determine eligibility for:

- the unused concessional contributions cap carry-forward

- the non-concessional contributions cap and the two- or three-year bring-forward period

- the government co-contribution

- the tax offset for spouse contributions

- SMSF to determine whether they can use the segregated assets method to calculate exempt current pension income.

- and used to match against events lodged on a TBAR

Each SMSF will now be required to provide for each member their 30 June:

- accumulation phase account balance. In SF360 this will be Accumulation accounts or Pension Accounts where the type is equal to TRIS.

- retirement phase account balance - capped defined benefit income streams. In SF360 this will be Pension Accounts where the type is equal to Complying Pension.

- retirement phase account balance – non-capped defined benefit income streams. In SF360 this will be Pension Accounts where the type is equal to Account Based Pension, Allocated Pension, Market Linked Pension and TRIS (Retirement Phase)

Three new labels (S1,S2 and S3) will be mandatory for each existing member. When added together these three fields must equal the existing closing account balance field.

- S1: Accumulation phase account balance

- S2: Retirement phase account balance – Non-capped defined benefit income streams (including market linked income streams)

- S3: Retirement phase account balance – Capped defined benefit income streams (Excluding market linked income streams)

It is now conditional as to whether the SMSF provides for each member their 30 June:

- Accumulation phase value

- Retirement phase value

Two new optional labels will be available to populate if it the amounts reported in the mandatory fields do not equal the definition of accumulation phase value or retirement phase value i.e. does not include the realised value. When populated, these amounts will be consumed for TSB purposes and the mandatory labels #1 and #2 (Accumulation phase account balance, and Retirement phase account balance – Non-capped defined benefit income streams will be ignored. The new Tax Return Labels are:

- X1: Accumulation phase value

- X2: Retirement phase value

The labels at X should be the superannuation benefits that would become payable from the members Accumulation and Retirement Phase Accounts (non-CDBIS only) if the member voluntarily caused the interest to cease. These values are allowed to be less than the amount the balances reported at label X as they may incorporate costs associated with exited the fund. These values should not be provided on a TBAR for the same financial year.

Transition to retirement income stream (TRIS)

You are now required to provide the number of open Transition to retirement income stream (TRIS) accounts in the accumulation phase for each member on 30 June 2018.

The TRIS is in accumulation phase unless the member has reached age 65 or has met another nil cashing restriction condition of release such as retirement, permanent incapacity, or terminal medical condition.

Foreign resident capital gains withholding tax

Changes to the threshold and withholding rate for foreign resident capital gains withholding apply to contracts entered into on or after 1 July 2017.

A 12.5% withholding obligation will apply to the disposal of:

- taxable Australian real property with a market value of $750,000 or more

- an indirect Australian real property interest

- an option or right to acquire such property or interest.

Where the vendor of these Australian assets is a foreign resident, the purchaser must pay 12.5% of the purchase price to the ATO as a foreign resident capital gains withholding payment.

A vendor can claim a credit for the foreign resident capital gains withholding payment the purchaser has made to the ATO by lodging a tax return for the relevant year.

How to deal with cryptocurrencies such as Bitcoin?

For more information see Tax treatment of cryptocurrencies and how to enter these in SF360 Click Here

Podcast - Changes to 2018 SMSF Annual Return

In episode 40 of the Smarter SMSF podcast, Aaron is joined by Jeevan Tokhi Product Manager at BGL to discuss the changes to the SMSF Annual Return (SAR) for 2017-18. The new superannuation reforms from 1 July 2017 has meant a raft of amendments to the current SAR that impacts member information such as total superannuation balances, and transition to retirement income streams (TRISs), along with updates to regulatory data including limited recourse borrowing arrangements and CGT relief information where a fund chose to defer under the transitional CGT relief provisions.

Aaron and Jeevan explore the impact of these specific changes, including what practitioners should be aware of when looking at the preparation of the financials and SMSF Annual Return for this income year.

Click Here to listen.

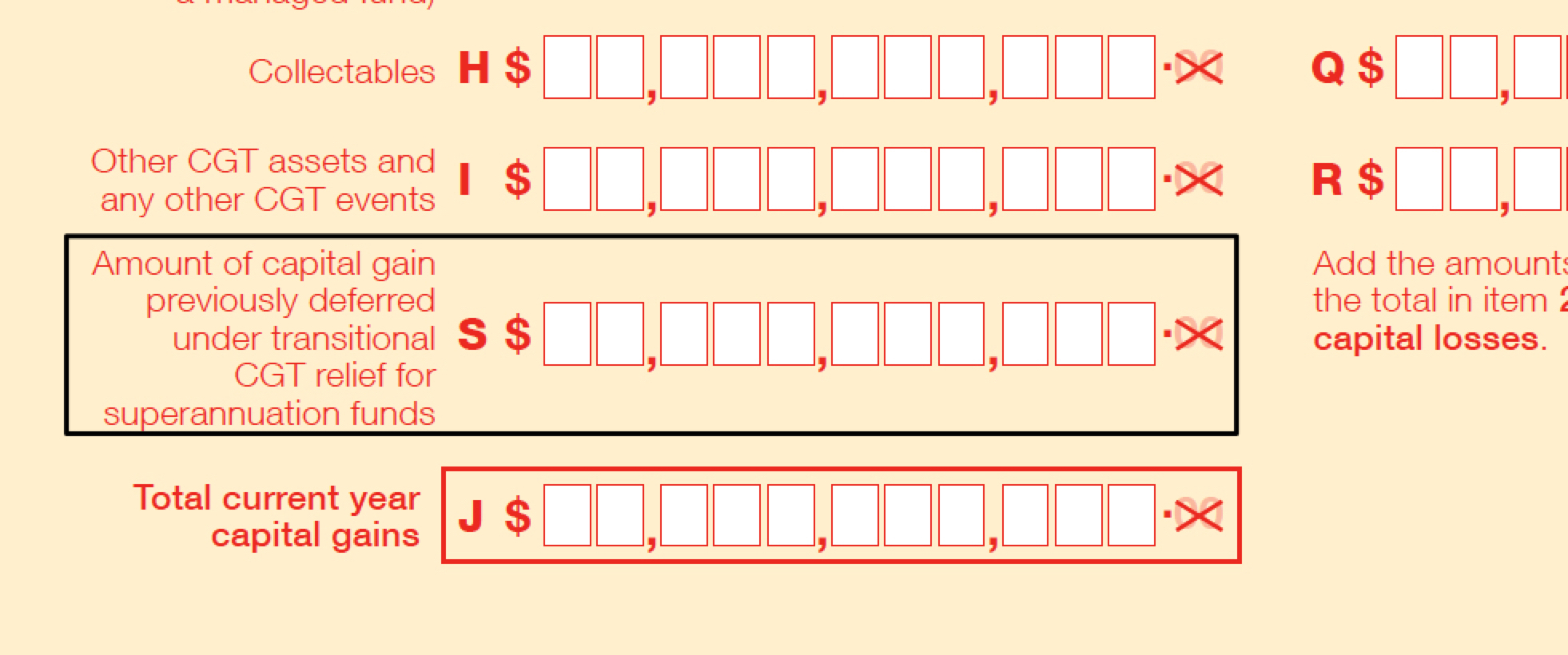

2018 CGT Schedule

CGT relief was also provided for certain SMSFs in the 2017 Financial year.

For the 2018 year onwards, where the SMSF has a deferred notional gain amount for an asset and that asset has been disposed of, the SMSF will need to report that the deferred notional gain has been realised in the CGT Schedule. The CGT Schedule must be lodged if a realisation event on an asset which has a deferred notional gain amount during 2017/2018.

This will also result in a change for the 'CGT method statement' and the Calculation of Net Capital Gains. When this asset is sold which has a deferred notional gain amount, the deferred capital gain is recognised. This deferred gain will not be discounted in the realisation year, however, it is to be reduced by capital losses made in that year as well as carried forward losses. Any exempt proportion e.g Actuarial Percentage applied for the realisation year e.g 2017/2018 does not apply to the deferred gain, as the relevant exempt proportion from the 2016/17 year was applied to this deferred gain.

Simple Fund 360 will automatically calculate the correct Net Capital Gain Amount and will populate the Capital Gains Schedule correctly.

SMSF Independent Auditor Report

There are no changes this year. Please refer to this excerpt from the ATO Website.

ECPI and Actuarial Certificates

As mentioned above, changes are currently in progress to support the Changes to ECPI from 01 July 2017 including part-year actuarial certificates.

From 1 July 2017, SMSFs can no longer use the segregated assets method to determine exempt current pension income where at any time during 2017-18 the SMSF had:

- at least one superannuation interest paying retirement phase superannuation income stream benefits, and

- at least one member who, just before 1 July 2017 had a total superannuation balance of more than $1.6million and was receiving retirement phase superannuation income stream benefits from any fund.

Furthermore, from 1 July 2017, SMSFs can only claim exempt current pension income where the current pension liabilities relate to the payment of retirement phase superannuation income stream benefits. This means SMSFs will have to pay tax on the earnings from assets supporting a TRIS where the recipient is under 65 and has not notified the SMSF they have met a condition of release with a nil cashing restriction (retirement, terminal medical condition or permanent incapacity).

The Pension Policies screen will be updated in Simple Fund 360 to support this.

TRIS will no longer eligible for ECPI

From 1 July 2017, income derived from assets supporting a TRIS will generally no longer be eligible for the pension earnings exemption. Earnings will now be taxed at 15% as a TRIS is generally not considered to be in the tax-free retirement phase.

However, there is an important exception to this rule, which applies where a fund member in receipt of a TRIS satisfies a specified condition of release with a nil cashing restriction (example reaching age 65).

Contributions

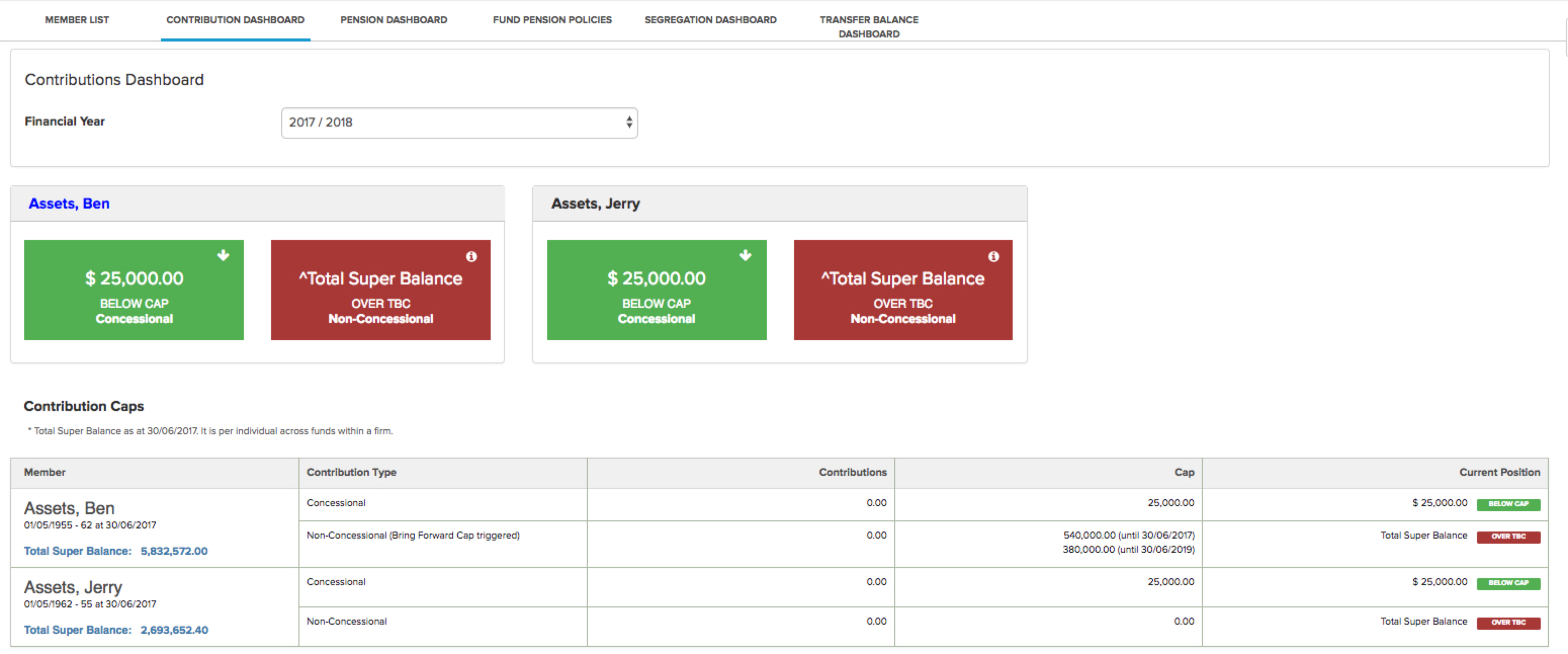

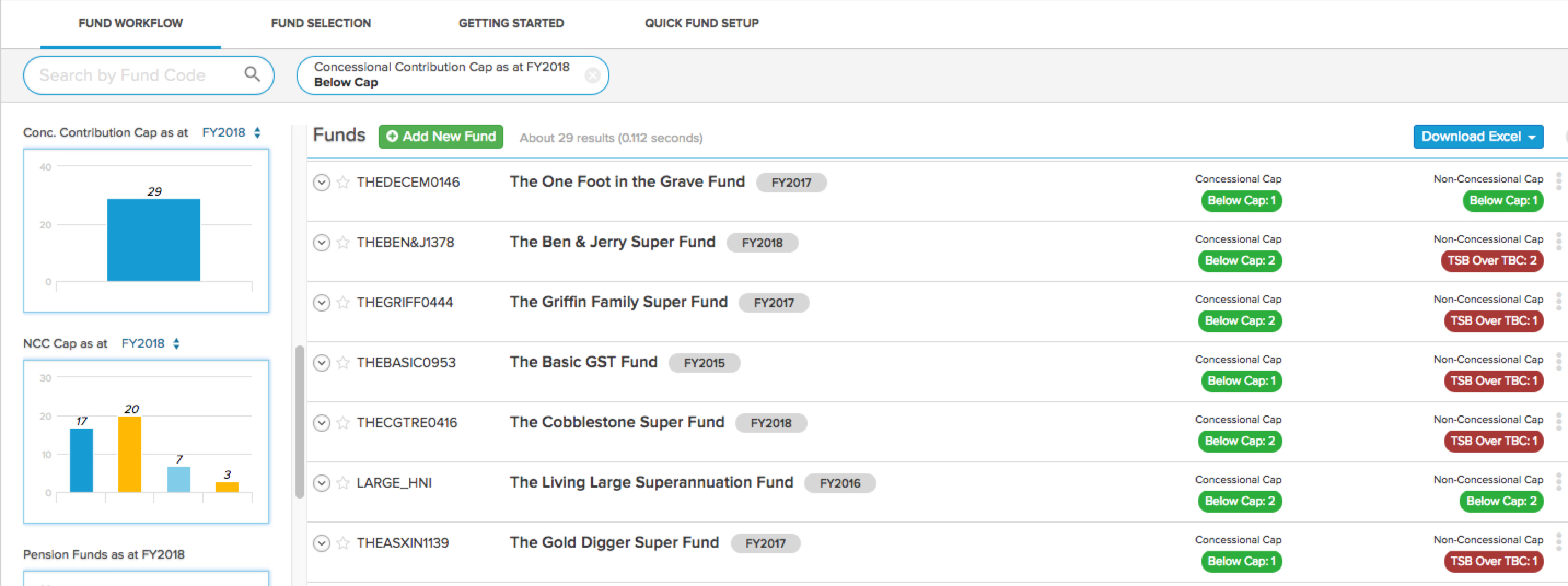

Concessional Contribution Cap changes

From 1 July 2017, the concessional contributions cap is $25,000 for everyone. Previously, it was $35,000 for people 49 years and older at the end of the previous financial year and $30,000 for everyone else.

The Contribution Dashboard for individual funds, Contribution Reports and Analytical Insights / Fund workflow screens which allow you to view contribution limits across all of your funds have all been updated to reflect the changes.

Non-Concessional Contribution Cap changes

From 1 July 2017, the annual non-concessional contribution cap reduced from $180,000 to $100,000 per year for the 2017-18 and future financial years. This will remain available to individuals aged between 65 and 74 years old if they meet the work test.

The major change also introduced is that the non-concessional cap is nil for a financial year if you have a total superannuation balance greater than or equal to the general transfer balance cap ($1.6 million in 2017–18) at the end of 30 June of the previous financial year. In this case, if you make non-concessional contributions in that year, they will be excess non-concessional contributions.

The Contribution Dashboard for individual funds, Contribution Reports and Analytical Insights / Fund workflow screens which allow you to view contribution limits across all of your funds have all been updated to reflect the changes

First Home Super Saver (FHSS) Scheme

From 1 July 2017 Individuals can make voluntary concessional (before-tax) and non-concessional (after-tax) contributions into their super fund to save for their first home. From 1 July 2018 the individuals meet the eligibility requirements can then apply to release the voluntary contributions, along with associated earnings, to help them purchase their first home.

Other Changes

A reminder that effective 1 July 2017, the 10% maximum earnings condition for personal super contributions deductions no longer applies for the 18 and future financial years.

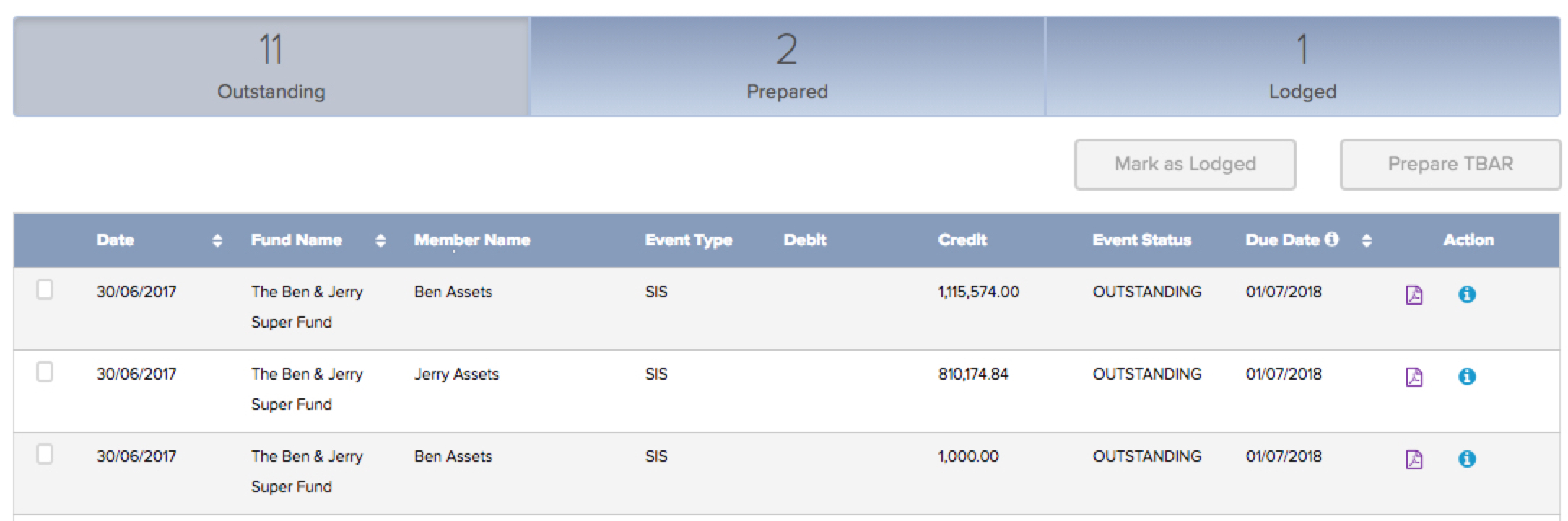

TBAR and Events Based Reporting

SMSFs in with at least one pension member have new reporting obligations. This is due to the new transfer balance cap measure and event-based reporting framework.

The transfer balance account report (TBAR) that is used to report is a separate form from the SMSF Annual Return. The TBAR enables the ATO to record and track an individual's balance for both their transfer balance cap and total superannuation balance for both SMSFs and large Superannuation funds.

The Transfer Balance Dashboard allows you to track an individual fund's reportable events, each member's transfer balance cap and generate a TBAR Form (PDF) to lodge to the ATO.

The TBAR Management allows you view and track TBAR events across all of your funds. On this screen you can create a bulk lodgement file for multiple members across all of your smsfs. You will be able to lodge ALL major TBAR events such as 30 June 2017 balances, pension commencements, pension commutations, Transition of TRIS to TRIS (Retirement Phase) and manually entered TBAR events.

This article was last updated on 10th July 2018