What's changed in the 2020 SMSF Annual Return

The following summarises changes to the SMSF Annual Return for 2020 compared to 2019.

The 2020 self-managed super fund (SMSF) annual return (SAR) form will be available at the end of May by the ATO and will include a number of changes.

Section A: Change to the auditor qualification question

You will be able to report 'No' at Part A qualification Label A when the audit report was qualified as a result of the auditor not being able to obtain sufficient audit evidence with respect to the SMSF's opening balances.

The ATO has stated that when a trustee signs the trustee’s declaration in the return, they confirm you have received the SMSF independent auditor’s report (IAR) and are aware of any matters it raises. A trustee who signs the return before receiving the IAR, you could face penalties of up to $12,600 for making a false and misleading statement.

Reporting whether issue/s have been rectified or not now applies to Part B qualifications only.

Section C: Deductions - Label removed - Anti-Detriment/Death Benefit Increase Deduction

From 1 July 2019, SMSFs can no longer claim a deduction for a tax saving amount paid on the death of a member. As a result, the Death Benefit Increase Deduction label has been removed. This change will ensure consistent treatment of lump sum death benefits across all super funds.

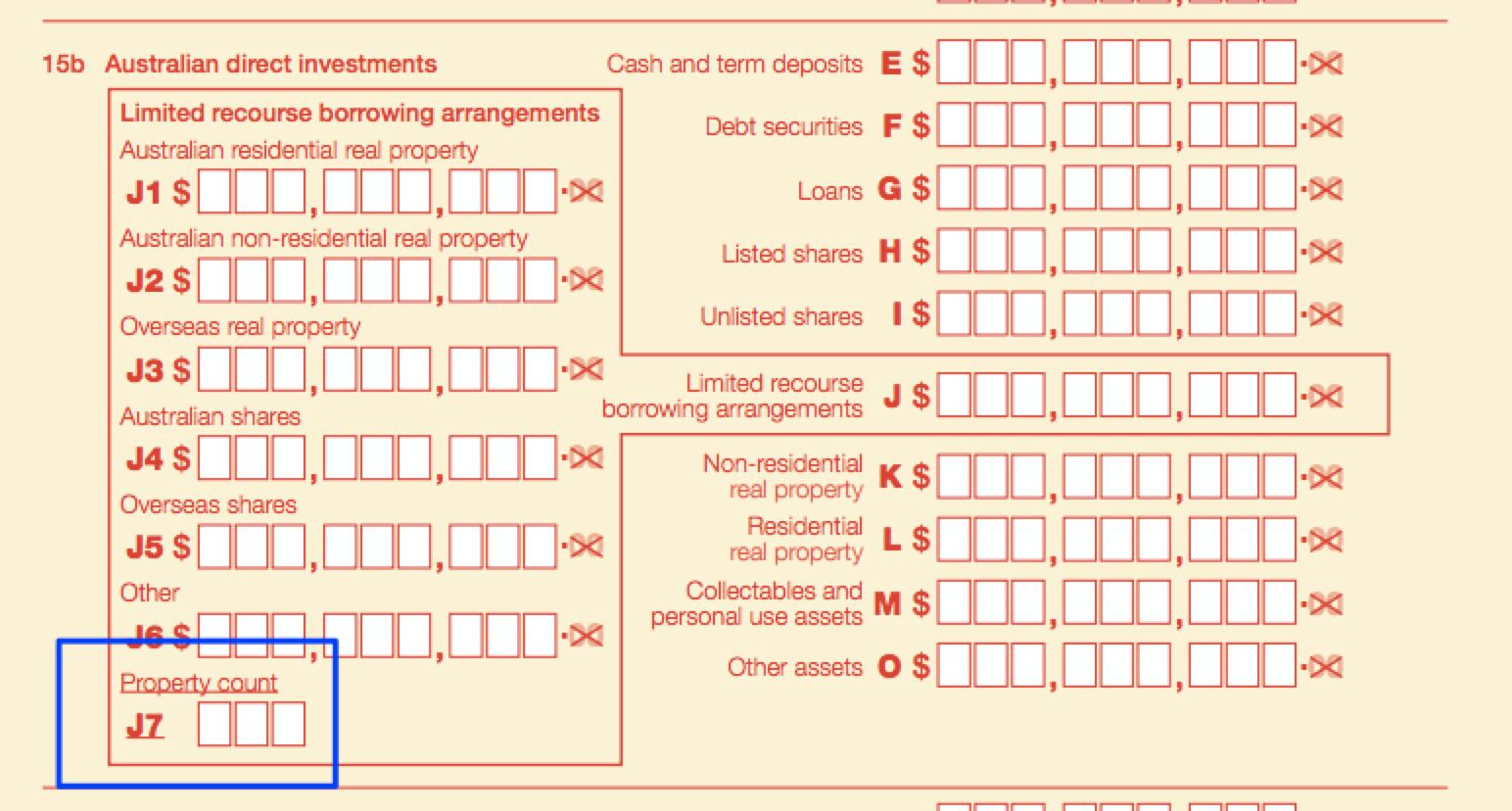

Section H: Assets & Liabilities - New label for Property Count

A label called Property Count will be added to Section H, Assets and Liabilities. This label will report the number of real properties your SMSF holds investments in that were held in trust as security under a Limited Recourse Borrowing Arrangement.

SMSF changes due to COVID-19 (novel coronavirus)

The ATO has announced measures based on the COVID-19 crisis including:

- Reduction in superannuation minimum payment amounts

- Temporary reduction in rent

- In-house asset restrictions

- Investment strategies

For further information see

- ATO Website - COVID-19 support available

- Simple Fund 360 Updates regarding the Economic Response to The Coronavirus

COVID-19 (novel coronavirus) – early release of superannuation

If a member of an SMSF is dealing with adverse economic effects of coronavirus, they may be able to access their super on compassionate grounds in certain circumstances.

From mid-April, eligible members can apply for a release of up to $10,000 of their super before 1 July 2020. They will also be able to access a further $10,000 from 1 July 2020 until 24 September 2020.

To apply for early release, the SMSF member must satisfy any one or more of the following requirements:

- They are unemployed.

- They are eligible to receive a job seeker payment, youth allowance for jobseekers, parenting payment (which includes the single and partnered payments), special benefit or farm household allowance.

- On or after 1 January 2020, either

- they were made redundant

- their working hours were reduced by 20% or more

- if they are a sole trader, their business was suspended or there was a reduction in their turnover of 20% or more.

Applications for early release of superannuation (super) will be accepted through myGov from 20 April.

You can register your interest now by logging in to your myGov account and following the Intention to access coronavirus support instructions.