Query

Is there a way to identify what holdings do not meet the 45 day holding period holding rule? That way I can quickly determine if dividends are not entitled to franking credits.

Background: Holding Period Rule

The holding period rule requires shares to be held ‘at risk’ for a continuous period of at least 45 days (90 days for preference shares) during the qualification period.

The 45-day and 90-day periods don't include the day of acquisition or, if the shares have been disposed of, the day of disposal. Also excluded are days where the financial risk of owning the shares is materially diminished. For example, the financial risk may be reduced through arrangements such as hedges, options and futures.

The primary qualification period begins the day after the shares are acquired, and ends 45 days after the ex-dividend date.

https://www.ato.gov.au/business/imputation/integrity-rules/franking-credit-trading/?anchor=Qualifiedpersontest#Qualifiedpersontest

If a shareholder purchases substantially identical shares over a period, the holding period rule applies a ‘last in first out’ method to establish which shares satisfy the holding period rule.

https://www.ato.gov.au/Business/Imputation/In-detail/Applying-the-last-in-first-out-method-under-the-holding-period-rule/

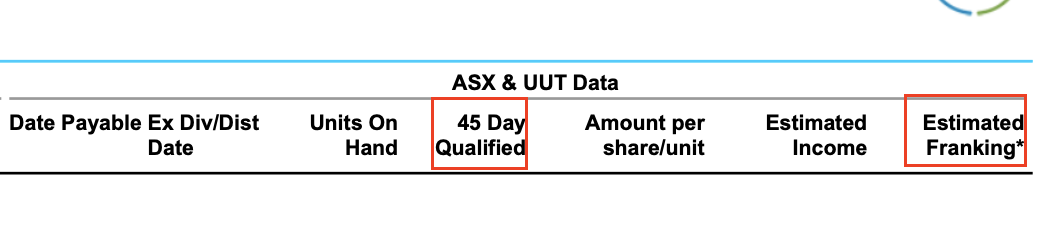

Holding Period Rule: How to find in Simple Fund 360

The number of units that Qualified for the 45 day holding rule is displayed in the Investment Income Comparison Report from within the Reports screen.

To access the Income Comparison Report, please take the following steps.

| Hover your cursor over Reports from the Main Toolbar, and select the Reports option from the pop-up menu. |  |

| Type 'Investment Income Comparison' into the search bar, or locate the Investment Income Comparison report under the heading Investment Reports. | |

| Add the report to the Report Pack List | |

| Select Preview Reports in the top right hand corner to view the Report. |

The 45-day holding period qualified units will be represented in the 45 Day Qualified column.

Estimated franking is updated by looking at qualified units under 45 day rule

Holding Period Rule: Calculation

The Holding Period Rule is calculated as follows:

Holding period = Disposal date - Purchase date -1

If the Holding Period is less than 45 days, the sell applied is unqualified and the remaining unit in the parcel is qualified.

Please note: Franking credit is estimated using 45 day qualified units. The estimation might not be accurate for preference shares and hedging arrangements.

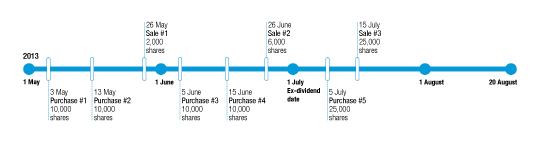

Please see the following example provided by the ATO.

Example 1: buying and selling multiple parcels of shares

The following example shows how to apply the holding period rule and the last-in first-out (LIFO) method. Follow these steps for the acquisitions and disposals of shares set out in the timelines below.

Step 1: Determine the group of shares on hand as at the ex-dividend date. The pre ex-dividend date sales are grouped and matched on a last-in, first-out basis.

.jpg?n=4227)

The group on hand as at the ex-dividend date is 32,000 shares. This is made up of:

- 4,000 shares on hand from purchase #4

- 10,000 shares from purchase #3

- 8,000 shares on hand from purchase #2

- 10,000 shares from purchase #1.

Step 2: Apply the LIFO method to the parcel of shares in sale #3 (sold after the ex-dividend date).

.jpg?n=747)

The result is that a franking credit entitlement is not available for purchase #4 (4,000 shares) and purchase #3 (10,000 shares). There is no loss of franking credits for purchase #1 and the balance of purchase #2. This is because these parcels have been held for more than 45 days applying the consistent LIFO methodology.

This means that unless other integrity rules apply, the entity can claim the franking credits attached to 18,000 shares (10,000 from purchase #1 and 8,000 from purchase #2).

https://www.ato.gov.au/business/imputation/in-detail/applying-the-last-in-first-out-method-under-the-holding-period-rule/