What is TWRR?

Time-weighted rate of return (TWRR) is a measure of the compound rate of growth in a portfolio over a specified time period.

it is the return generated when you invest $1 at the beginning of the period while no money is added or taken out since then.

How to Calculate TWRR?

Assumptions / Notes

-

The market price of the investment will always be fully adjusted when an income/instalment/ return of capital is incurred.

e.g. If the market price of a share is $2.00 right before a dividend of $0.05 per share is paid, the post-dividend price will be $2.00 - $0.05 = $1.95.

-

Income / Instalment / Return of capital incurred at ti are only related to the beginning holdings at ti.

-

Unit price will be calculated based on the cost base of the investment if no market price is available (e.g. non-unitised investment).

-

Unit change resulting from corporate actions (i.e. bonus issue / share split / share consolidation) is not considered in the TWRR calculation at the current stage.

-

The Fund’s TWRR includes returns from all bank accounts, unitised investments and non-unitised investments held by the Fund.

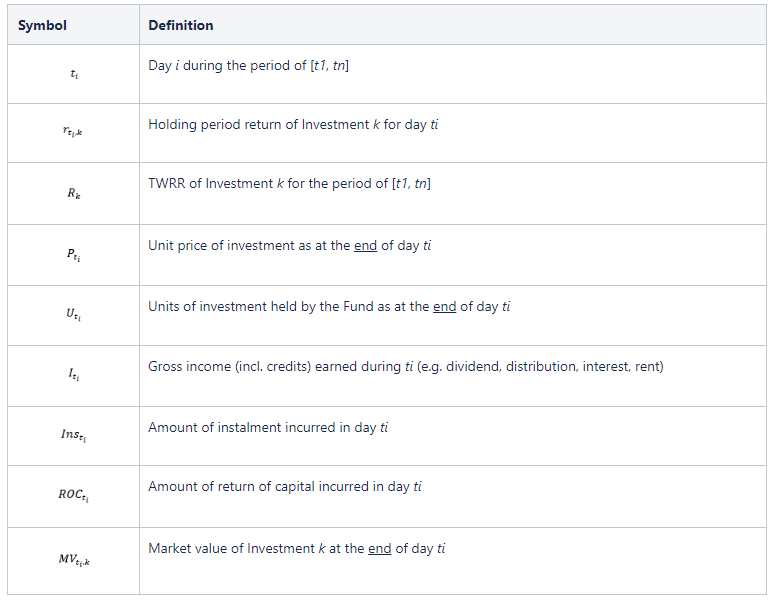

Symbol Definition

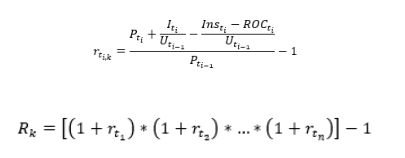

Return for Individual Investment (Sub Account Level)

-

We first break the whole period down into multiple sub-periods (one day in our calculation) and then calculate the holding period return for each sub-period. The TWRR is then calculated as the geometric mean of all holding period returns.

-

Formula:

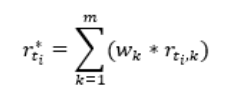

Return for Portfolio (Control Account / Fund Level)

-

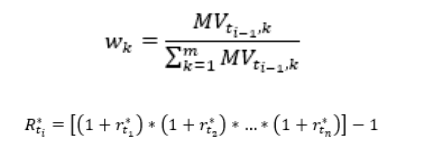

The holding period return of the portfolio for a particular sub-period is a weighted average of individual holding period returns for that sub-period, with the weight being the beginning market value of the Investment k as a fraction of the total beginning market value of the portfolio. And similar to the individual investment, the TWRR of the portfolio is calculated as the geometric mean of the holding period returns of the portfolio.

-

Formula:

where

Why TWRR?

-

Global Investment Performance Standards (GIPS para 2.A.2) requires the return to be calculated by TWRR (see attachment for more information).

-

TWRR captures the overall portfolio performance rather than the performance due to individual security-level decisions. It provides a whole picture to the trustees when they are doing the retirement planning.

-

Unlike money-weighted rate of return (MWRR), TWRR does not take the impact (i.e. size and timing) of cash inflows / outflows into account and thus it eliminates the distorting effects on growth rates created by cash flows. Accordingly, TWRR is a more appropriate measure to be applied when:

- judging the performance of those financial advisors / fund managers who have NO control over the amount and timing of flows

- evaluating the asset allocation of the Fund

- benchmarking the Fund’s return against general market returns

-

The algorithm of TWRR is simpler than that of MWRR for portfolios (Funds) with smaller but more frequent contributions / withdrawals.

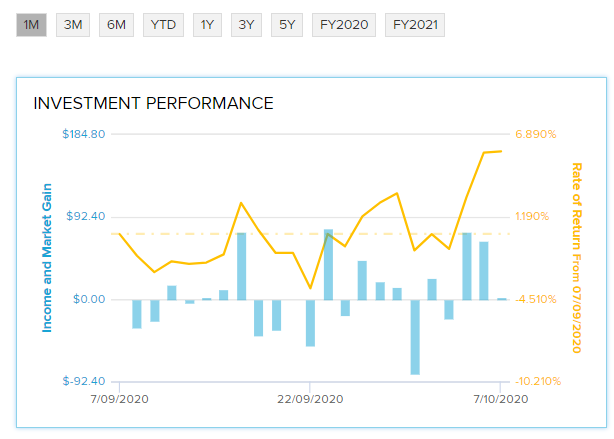

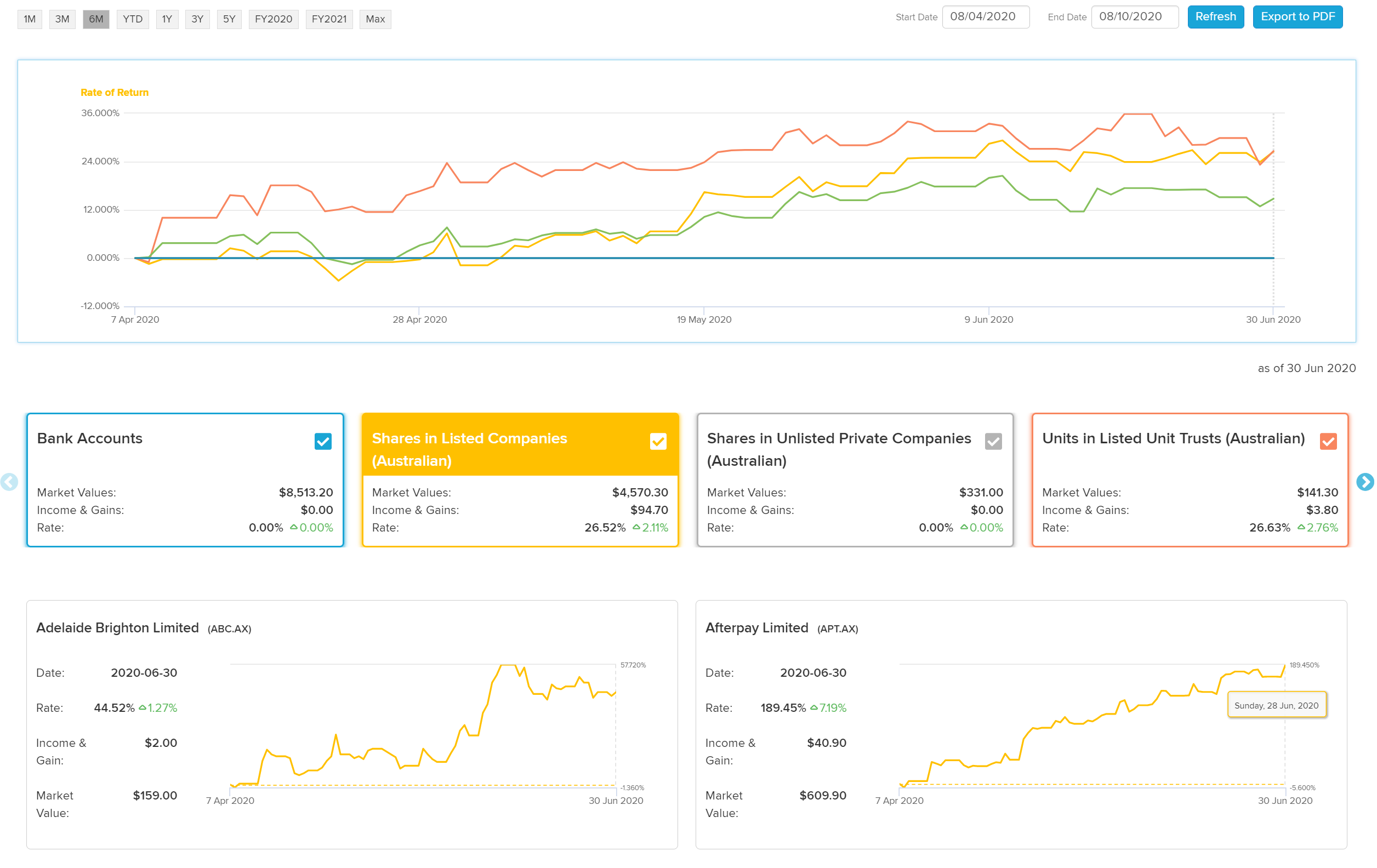

Navigation

| From the Main Toolbar, navigate to Investments. |  |

| Select Investment dashboards |

|

The TWRR will display under both the Dietz Performance and Time Weighted Performance tab.

.

.