The following summarises changes to the SMSF Annual Return for 2019 compared to 2018.

Fund Details - SMSF auditor

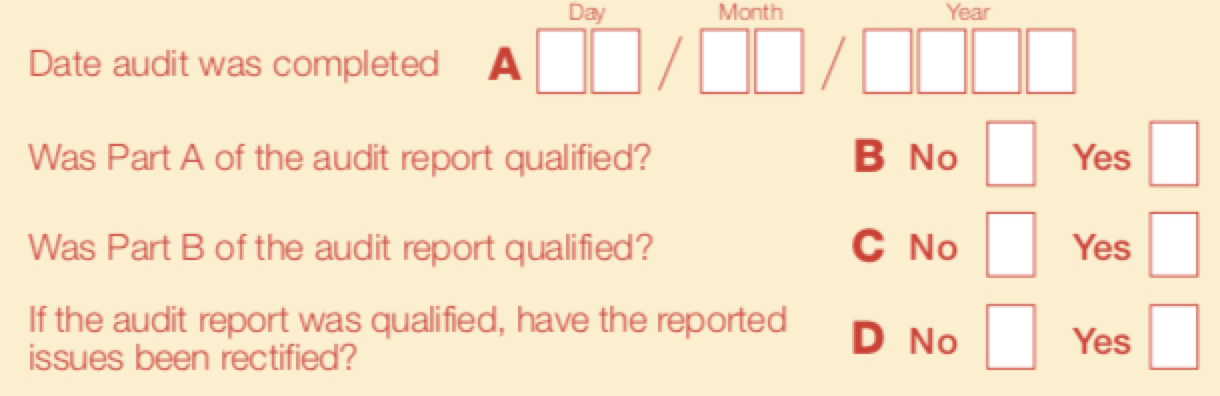

A new label B has been added: "Was Part A of the audit report qualified?". This label is to report the Part A qualification outcome determined by the fund's SMSF Approved Auditor.

In prior years, you were asked whether Part B of the audit report was qualified. The 2019 SMSF annual return will also ask whether Part A of the audit report was qualified. Part B of the auditor’s report gives the auditor’s opinion on the fund’s compliance with super laws and Part A of the report gives the auditor’s opinion on whether the fund’s financial statements are fairly presented (ie there are no material misstatements).

You must now answer 'yes' if the audit report was qualified at Part A and/or Part B, regardless of the auditor's reasons for the qualification. In prior years the ATO advised you could answer 'no' if the only reason the auditor qualified Part B was that they could not confirm the information provided to them (for example, opening account balances). This is no longer the case. Your answers must correctly convey the auditor's written opinion.

This information will the ATO build a more complete risk profile of the SMSF population.

Fund Details - Bank Account and ESA changes for SuperStreame

Several changes will be made between over the next few years to include SMSFs into SuperStream for rollovers. From the 2018-2019 year onwards:

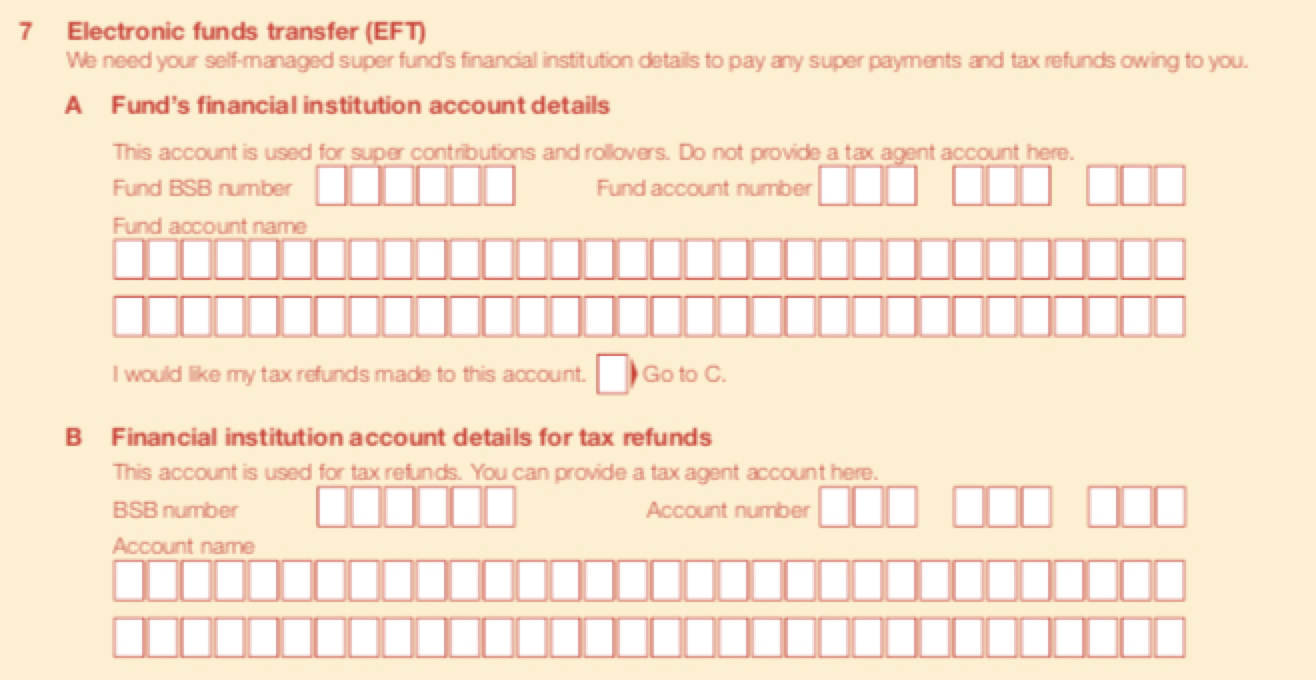

- The title has been updated to “Fund’s financial institution account details”

- The instructive text has been updated to: This account is used for super contributions and rollovers. Do not provide a tax agent account here.

- Label 7a will be mandatory to complete

- A new checkbox is to be displayed within Section A label 7a named "I would like my tax refunds made to this account. Go to C". If the checkbox is selected, then Section A Fund Information label 7b does not need to be completed

- The Account name now allows up to 200 characters (including spaces).

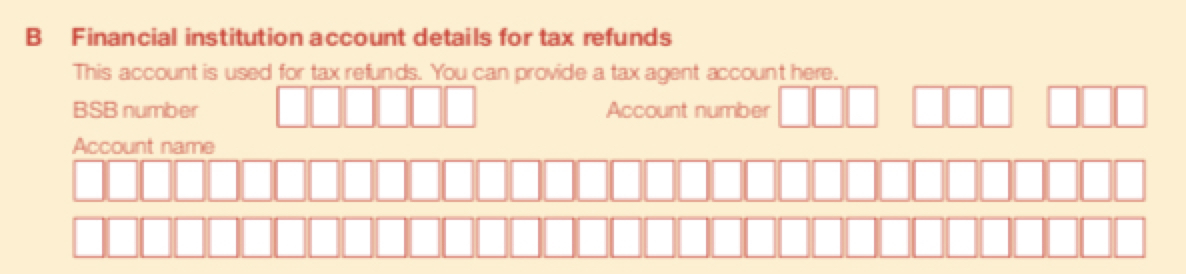

Changes to Section A label 7b - Financial Institution account details for tax refunds

- a) The title for label 7b has been updated to: “Financial Institution account details for tax refunds”

- Label 7b instructive text has been updated to: "This account is used for tax refunds – you can provide a tax agent account here."

- The Account name now allows up to 200 characters (including spaces).

- The details entered at label 7b must be different from those entered at label 7a

Members - Downsizer Contributions

In the 2017-18 Budget, the Government announced the contributing the proceeds of downsizing to superannuation measure to reduce pressure on housing affordability. This law has been passed which allows individuals to use the proceeds in relation to one sale of their main residence to make contributions (downsizer contributions) of up to $300,000 to their superannuation provider if they are 65 years of age or over and meet all the eligibility requirements. Downsizer contributions can be made regardless of the other contributions caps and restrictions that might apply when making voluntary contributions.

See Downsizer Contributions for to enter these contribution types into Simple Fund 360.

For the 2018-19 financial year onwards the Members Section will display the Downsizer amount to be reported along with the date in which the event took place.

An SMSF Annual Return will fail the ATO's validation if the contribution amount reported is greater than $300,000, there is a receipt date but no contribution amount or there is a contribution amount but no receipt date.

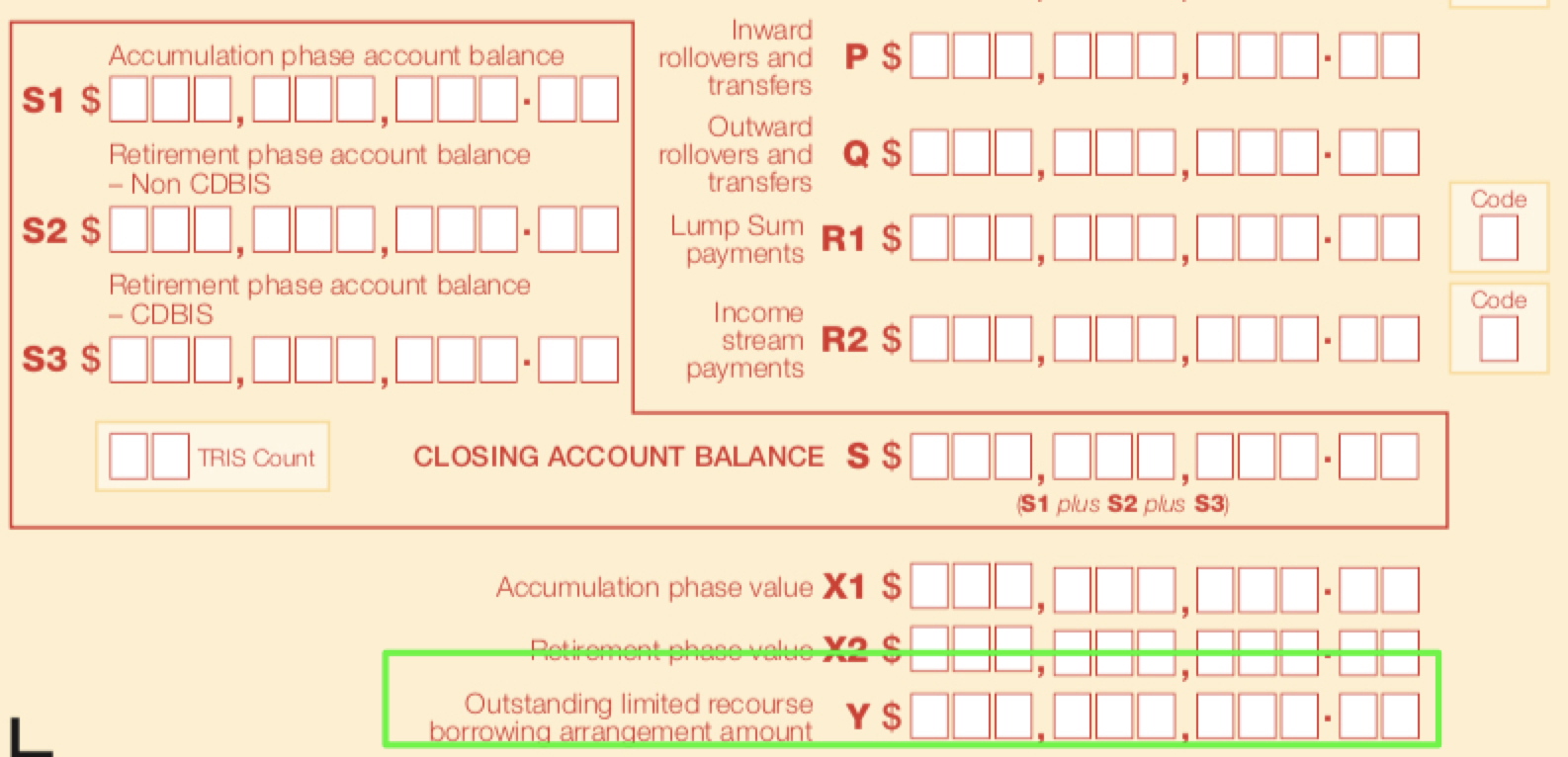

Members - LRBAs

A new label has also been added to the Member sections of the 2019 SMSF annual return to report the outstanding LRBA amounts for each member. This information will be used for statistical purposes only. You should report the outstanding loan balances for all LRBAs, and not just those that would have been caught by the proposed changes for total superannuation balance purposes. The reported amounts will not be used in calculations of a member’s total superannuation balance.

The ATO will accept any reasonable method of calculating the amount to report. The following methodology, which aligns to the proposed changes under Subsection 307-231(3) of Treasury Laws Amendment (2018 Superannuation Measures No. 1) Bill 2018External Link is one such acceptable method:

Member's outstanding LRBA = Fund's outstanting LRBA * (value of member's interest supported by the assets that secure the LRBA) / (value of fund's interests supported by the assets that secure the LRBA).

From 2018-19 financial year onwards:

- A new label “Y” has been added to the SMSF annual return in the Members information Sections F and G after Closing account balance, named “Outstanding limited recourse borrowing arrangement”

- An error will be triggered when the total of amounts reported at the new LRBA label ‘Y’ for all members is greater than the amount reported at Section H Liabilities label V1 “Borrowings for limited recourse borrowing arrangements”

Assets and Liabilities - Cryptocurrencies

A change has also been made to the way crypto-currency is reported in the Assets section of the 2019 SMSF annual return. Crypto-currencies, which were previously reported at the 'Other overseas assets' label, will now be reported at a dedicated Crypto-currency label.

The term crypto-currency is generally used to describe a digital asset in which encryption techniques are used to regulate the generation of additional units and verify transactions on a blockchain. Crypto-currency generally operates independently of a central bank, central authority or government.

'Crypto-Currency' in the SMSF Annual return refers to Bitcoin, or other crypto or digital assets that have the same characteristics as Bitcoin. The characteristics of Bitcoin are set out in TD 2014/25.

Refer to How to deal with cryptocurrencies such as Bitcoin? for how to enter transactions and set up the Chart of Accounts in Simple Fund 360. If you have added a Custom Account for this in the Chart of Accounts ensure you have selected the correct Tax label.

The ATO is collecting bulk records from Australian cryptocurrency providers as part of a data matching program to ensure people trading in cryptocurrency are paying the right amount of tax

ATO References