Overview

If a fund has ECPI and Tax Losses (both carried forward from previous periods and current amounts), Simple Fund 360 applies the Tax Losses in the following way:

- The Tax Loss is first reduced by the Net ECPI of the fund, where Net ECPI = ECPI - Non deductible expenses.

- The Taxable Income for the fund is then reduced by any amounts of Tax Loss remaining from the previous step.

- If the Tax Loss exceeds the Taxable Income for the fund, any remaining amounts of Tax Loss from the previous step can be carried forward.

Reports

Use the below table to both reconcile the following amounts and find their SMSF Annual Return locations:

| Amount | Report | Label |

|---|---|---|

| Exempt current pension income (ECPI) | Exempt Pension Reconciliation | Section B Item 11 Label Y |

| Non deductible expenses | Pension Non Deductible Expense Report | Section C Item 12 Label Y |

| Taxable income | Detailed Operating Statement | Section C Item 12 Label O |

| Tax losses deducted | Tax Reconciliation Report | Section C Item 12 Label M1 |

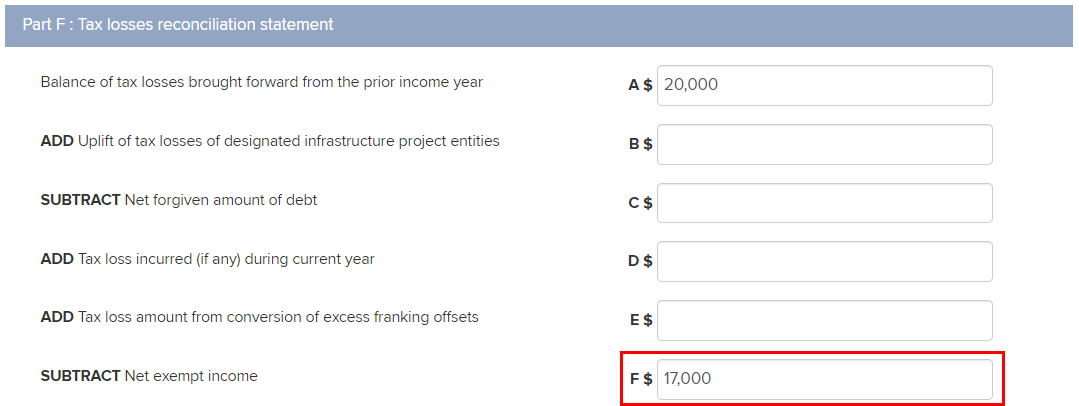

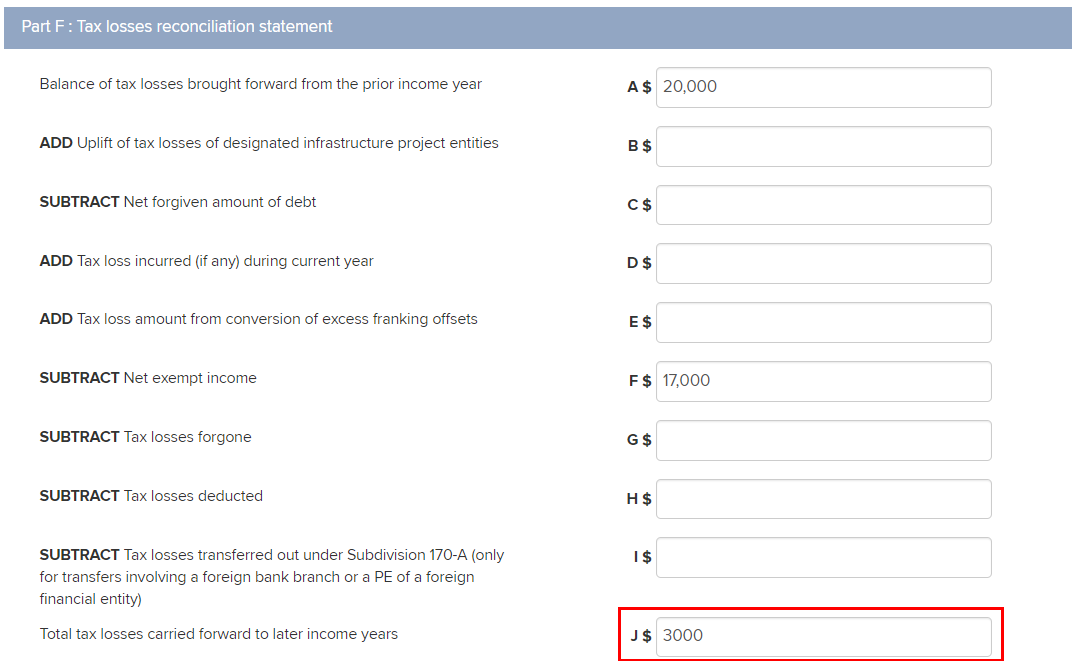

Example

1. A client had $20,000 in carry forward tax losses.

2. $17,000 was applied to the Net Exempt Income which is calculated as ( Exempt Current Pension Income - Non Deductible Expenses).

To further investigate the calculation, the Exempt Current Pension Income can be found in the Exempt Amount column total within the Exempt Pension Reconciliation report.

The Non Deductible Expense can be found in the Non Deductible column total within the Pension Non Deductible Expense report.

3. The remaining $3,000 has been carried forward to be applied to future Net ECPI.

.