Overview

The steps below can be followed to convert a TRIS to a TRIS - Retirement Phase.

From 1 July 2017, the pension earnings exemption has been completely removed for income derived from assets supporting a TRIS.

This means that any income derived when a member is in TRIS phase will be taxed at the fund tax rate (15%).

A TRIS - “Retirement Phase” was introduced as part of the reform for members to obtain the pension earnings exemption in certain circumstances:

- Meeting the condition of release of ‘retirement’;

- Meeting the condition of release ‘permanent incapacity’;

- Meeting the condition of release ‘terminal medical condition’;

- Attains age 65 and satisfies a 'nil' cashing restriction.

This Retirement Phase interest comprises pension interests that are of a tax-free nature and will have an effect on a member's personal Transfer Balance Account; in contrast to a TRIS which is not comprised of amounts in the tax-free environment.

When is a TRIS eligible to convert to the Retirement phase?

With reference to the Income Tax Assessment Act 1997 s307-80:

307-80(1)

A *superannuation income stream is in the retirement phase at a time if a *superannuation income stream benefit is payable from it at that time.

307-80(2)

A *superannuation income stream is also in the retirement phase at a time if:

(a) it is a *deferred superannuation income stream; and

(b) a *superannuation income stream benefit will be payable from it to a person after that time; and

(c) the person has satisfied (whether at or before that time) a condition of release specified in any of the following items of the table in Schedule 1 to the Superannuation Industry (Supervision) Regulations 1994:

(i) 101 (retirement);

(ii) 102A (terminal medical condition);

(iii) 103 (permanent incapacity);

(iv) 106 (attaining age 65).

However, it is important to note that under s307-80(b)(ii) that the TRIS is not in the Retirement Phase unless the member has notified the trustee of the SMSF that a condition of release has been met.

Instructions

| From the Main Toolbar, go to Member. |

|

| Select Member list. |

|

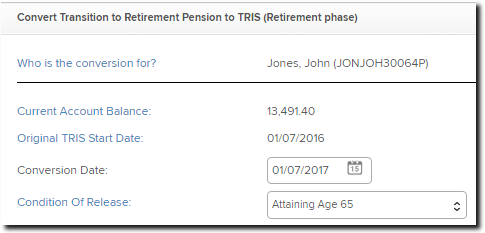

- Select Convert to TRIS (Retirement Phase) next to the relevant TRIS member.

- Input the conversion date. This will present the balance to convert. If this change is partway through the year, you will need to complete the Create Entries Process up until the day before the change.

- Confirm the rollover and preservation components. Select Save and Prepare Documents to proceed with the conversion and to prepare documentation.

- A TRIS - Retirement Phase conversion will impact a member's Transfer Balance Cap. Refer to Transfer Balance Dashboard for more.

TRIS Pension Conversion Letter/Minutes

Select Save and Prepare Documents to produce the TRIS Conversion Letter/Minutes. These can also be prepared from the Reports screen at a later stage.

- From the Main toolbar, select Report.

-

From the Reports screen, under the Letters/Minutes section, click the arrow on the right next to the TRIS Pension Conversion Letter/Minutes.

- Select Preview to download the documents. These documents can also be included as part of a Report Pack.

Reverse a TRIS to TRIS - Retirement Phase.

Reversing an account from a TRIS in Retirement Phase to a TRIS can be completed in the Member List screen.

| From the Main Toolbar, go to Member. |

|

| Select the Member list. |

|

- Locate and select the member's account by clicking anywhere highlighted below:

- Change the Pension Type to Transition to Retirement Pension. Also ensure the Account Description is updated accordingly:

Note: This process can also be used to edit a member's pension type.

- Scroll down, then click Save to complete the process.