- Remove the tax exempt status of income from assets supporting a Transition to Retirement Income Stream (TRIS);

- Individuals will no longer be allowed to treat certain superannuation income stream payments as lump sums for tax purposes;

- Full or partial commutations of superannuation income streams will be treated as superannuation lump sums.

Comparison of key features of new law and current law

See also: TRIS vs TRIS in Retirement Phase

|

New law

|

Current law

|

|

|---|---|---|

| Earnings tax exemption provisions |

|

|

| TRIS when a condition of release is met |

|

|

Opportunities/Planning in Simple Fund 360

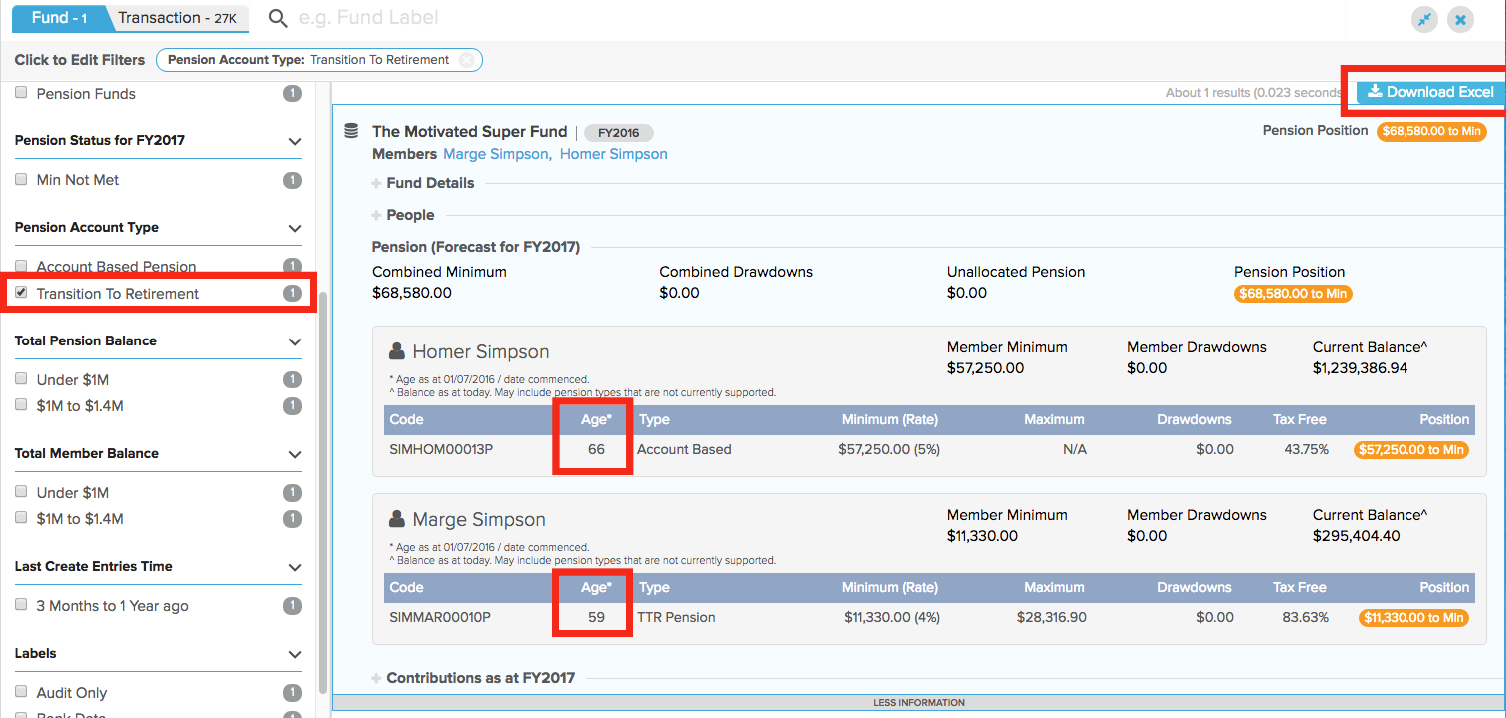

- SMSFs which currently have a Transition To Retirement pension can be easily identified using the Analytical Insights screen.

- Members' ages can be obtained on-screen or by downloading a list of filtered funds to Excel.

What do I have to do in Simple Fund 360 from 30/06/2017?

I want to continue the TRIS, however, I understand it now is not in Retirement Phase. Do I have to move the TRIS from Pension to Accumulation?

If the Pension will continue in the 2018 FY there is nothing additional you need to do.

- For Unsegregated Funds, the Create Entries process will treat the TRIS account the same as an accumulation account.

- For Segregated Funds, assets allocated to a TRIS account will be treated as taxable

I will be partially or fully commuting the TRIS as at 30/06/2017 to comply with the Transfer Balance Cap. What do I need to do?

Refer to Commuting pensions before 1 July 2017 to avoid exceeding the $1.6 million transfer balance cap

How do I convert a TRIS to an Account Based Pension?

Refer to How to convert a TRIS to an Account Based Pension

What will happen for TRIS's and application for Actuarial Certificates in 2018?

If the fund only has non-retirement accounts (e.g Accumulation and Pension accounts) there will be no need to apply for an actuarial certificate.

For funds which have a mixture of Retirement and Accumulation accounts the following will occur for Actuarial Certificate application in SF360 for FY2018 onwards

- TTR/TRIS pensions will be recorded as accumulation interests

- A pension payment from a TRR/TRIS will be shown as an accumulation withdrawal

- A conversion from TTR/TRIS to a full ABP or a TRIS (retirement phase) will be shown as a pension commencement

- A commutation/rollback of a TTR/TRIS to accumulation will not be submitted

How do I monitor a member's Transfer Balance Cap?

Refer to Transfer Balance Dashboard