Where individuals need to commute superannuation income streams to transfer amounts from the retirement phase to the accumulation phase to comply with the transfer balance cap, earnings on assets supporting these commuted balances will become taxable.Similarly, where individuals have a TRIS, earnings on assets supporting these superannuation income streams will become taxable from 1 July 2017 as they will no longer be in the retirement phase.

The CGT Relief provide relief for Self-Managed Superannuation Funds (SMSFs) from the tax consequences for capital gains accumulated before 1 July 2017 where these gains would have been exempt income if realised prior to a commutation being made to comply with the transfer balance cap or the change to the treatment of TRIS. The assets must be held during the pre-commencement period of 9 November 2016 to just before 1 July 2017 in order to be eligible.

The superannuation fund must choose to apply the relief if they wish to do so which are:

- the choice to reset the cost base of a CGT asset to its market value when the asset ceases being a segregated current pension asset during the pre-commencement period, but is held by the fund throughout that period

- the choice to reset the cost base for an unsegregated CGT asset to its market value on 30 June 2017, where the fund holds the asset throughout the pre-commencement period.

CGT relief is not automatic. The trustee of a complying superannuation fund must choose for CGT relief to apply for a CGT asset. The choice is irrevocable and must be made on or before the day a trustee is 'required to lodge' their fund's 2016-17 income tax return.

Comparison of key features of new law and current law

|

New law

|

Current law

|

|---|---|

|

|

Opportunities/Planning in Simple Fund 360

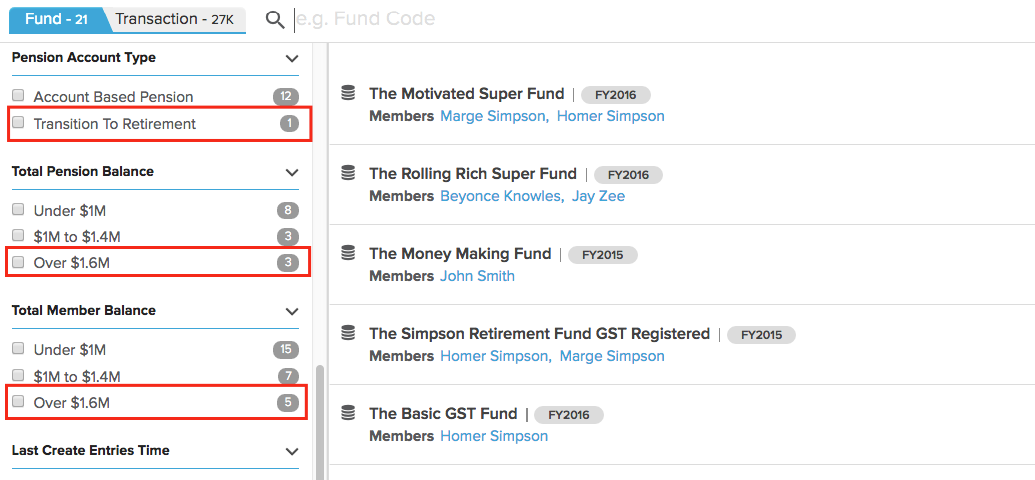

- The Analytical Insights screen can be used to filter and identify which SMSFs have pension members with a balance over $1.6 million and which funds have a TRIS.

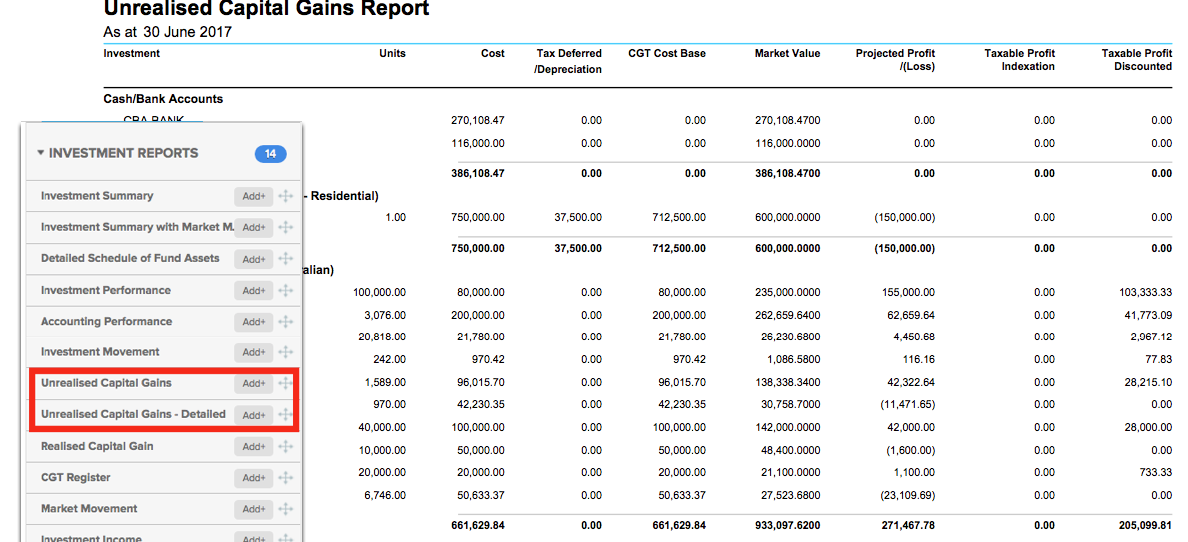

2. For those funds identified, the Unrealised Capital Gains Report and Unrealised Capital Gains Report - Detailed can be used to identify which assets which CGT Relief would be suitable for.

Determine which option of CGT relief is best for each asset or parcel:

- This could be choosing which assets to reset their cost base and paying any capital gain tax.

- It may be choosing which assets to reset their cost base and deferring any capital gain tax.

- Or it may be choosing not to reset any asset cost base and not applying for CGT relief.

Record the Transitional CGT Relief (Cost base reset)

You can apply CGT relief to the fund's assets in Simple Fund 360 through the Corporate Actions screen.

Refer to How to record Transitional CGT Relief (Cost base reset) for further instructions.

The following documents are also now available in Simple Fund 360: