From 1 July 2017, the government will make the following changes:

- the annual concessional contributions cap will reduce to $25,000 (from $30,000 for those aged under 49 at the end of the previous financial year and $35,000 otherwise); and

- the threshold at which high-income earners pay Division 293 tax on their concessionally taxed contributions to superannuation will reduce to $250,000 (from $300,000).

Comparison of key features of new law and current law

| New law | Current law | |

|---|---|---|

| Annual concessional contributions cap |

The cap on concessional contributions for a financial year is $25,000 for all individuals. The cap is indexed and increases in increments of $2,500 in line with average weekly ordinary time earnings (AWOTE). |

The cap on concessional contributions for a financial year is: • $30,000 for individuals aged under 49 years at the end of the last financial year; and • $35,000 for individuals aged 49 and over at that time. The $30,000 cap is indexed and increases in increments of $5,000 in line with AWOTE. |

| Division 293 tax threshold | Division 293 tax applies to an individual for an income year if the total of the individual’s combined income for surcharge purposes and concessionally taxed contributions exceeds $250,000. | Division 293 tax applies to an individual for an income year if the total of the individual’s combined income for surcharge purposes and concessionally taxed contributions exceeds $300,000. |

Opportunities/Planning Simple Fund 360

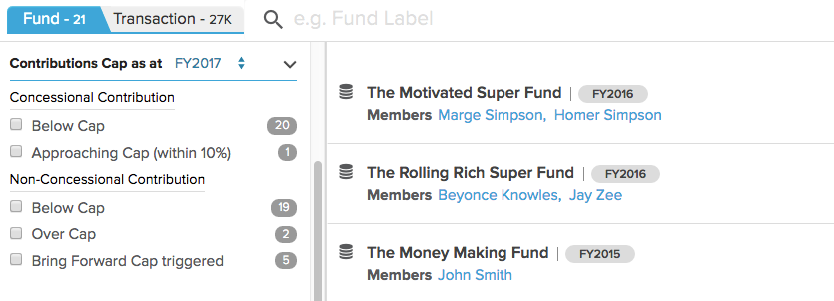

- Use the Analytical Insights to identify funds currently at or approaching Concessional Cap limits to assist in identifying Members who currently contribute more than $25,000. These funds will need further review to their current Contribution or existing Salary Sacrifice arrangements.

Changes to Simple Fund 360

- Changes to the Contribution Dashboard, Contribution Reports and Analytical Insights will be added during 2017.