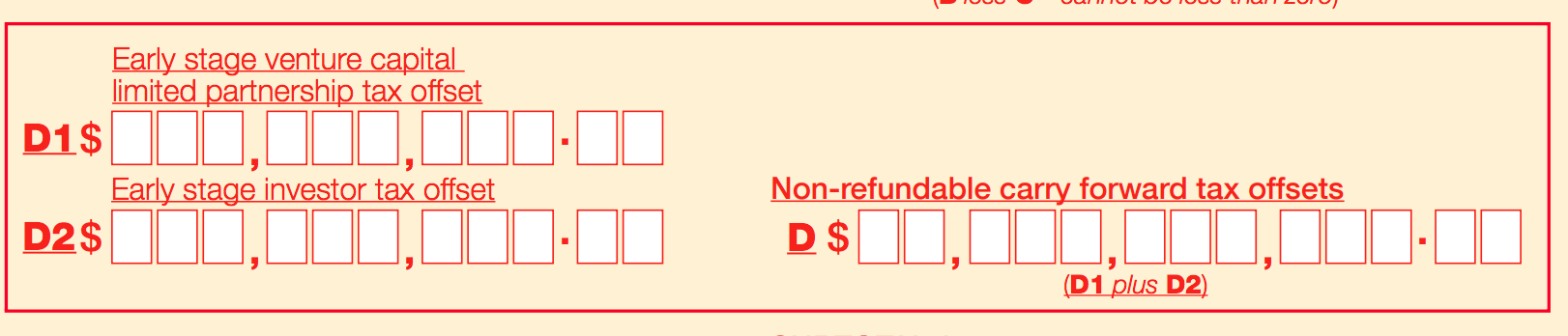

Section D: Income tax calculation statement - Early stage venture investor offsets and Non-refundable carry forward tax offsets

D1: Early stage venture capital limited partnership tax offset

From 1 July 2016, an SMSF that is a limited partner of an early stage venture capital limited partnership (ESVCLP) may qualify for:

- a non-refundable carry forward tax offset of up to 10% of their contribution to an ESVCLP. The ESVCLP must have become unconditionally registered on or after 7 December 2015. This includes an ESVCLP that was conditionally registered before this time and then became unconditionally registered on or after 7 December 2015.

- a tax exemption for part of the capital gain or income from the disposal of investments that accrued to the end of the period ending six months after the end of an income year in which the investee’s value has first exceeded $250 million.

The ESVCLP tax offset is shown at D1

D2: Early stage investor tax incentives

From 1 July 2016, investors who acquire newly issued shares in a qualifying n eligible qualifying Australian early stage innovation company (ESIC) may qualify eligible for:

- a tax offset equal to 20% of the amount paid for the shares. This tax offset is capped at a maximum amount of $200,000 for each income year for the investor and their affiliates combined. The offset is not refundable, but can be carried forward to the next income year.

- a modified CGT treatment under which the investor can disregard any capital gains made on the shares that have been continuously held for between one and ten years. an exemption from CGT on shares continuously held by the investor for between one and ten years. Any capital losses on the shares held for less than ten years must be disregarded.

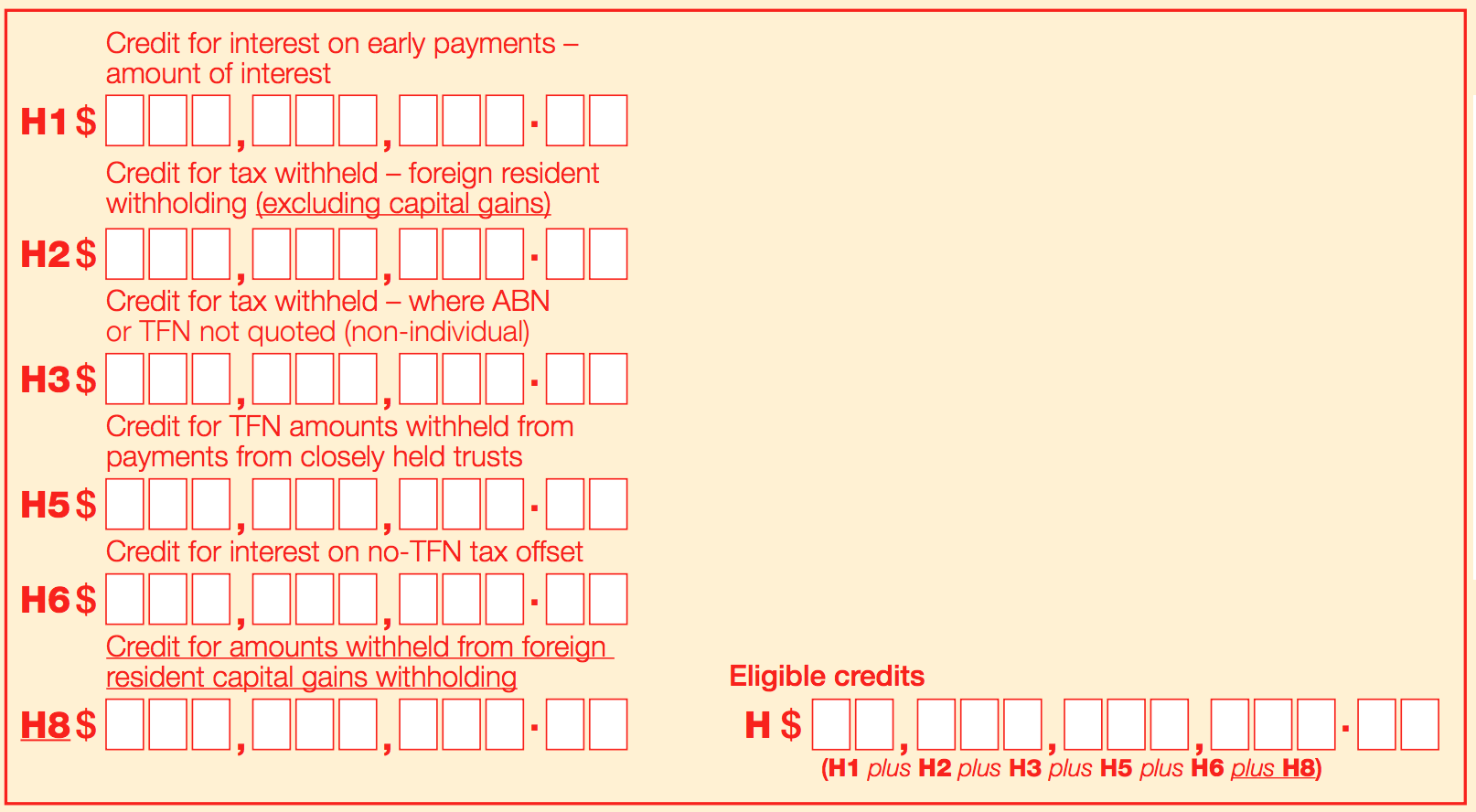

Section D: Income tax calculation statement - Eligible Credits

- New label (H8), added

- Label H2 descriptor and label H descriptor at Q13 updated

- Refer to ATO - Capital gains withholding: Impacts on foreign and Australian residents

H2 Credit for tax withheld – foreign resident withholding

Write at H2 the total amount of tax withheld from payments to the SMSF that were subject to foreign resident withholding in Australia. Include at H2 the SMSF’s share of foreign resident withholding credits distributed to the SMSF from a partnership or included in a share of net income from a trust.

If a payer has withheld tax for foreign resident withholding from a payment to the SMSF, the payer must give the SMSF a payment summary that shows how much the payer withheld from its payments to the SMSF.

H8 Credit for amounts withheld from foreign resident capital gains withholding

Write at H8 the total amount of tax withheld from payments to the SMSF that were subject to foreign resident capital gains withholding in Australia. Include at H8 the SMSF’s share of foreign resident capital gains withholding credits distributed to the SMSF from its share of net income from a trust. You should only claim at H8 a credit equal to the amount of foreign resident capital gains withholding paid by a purchaser to the ATO on your behalf. The ATO would have issued you with confirmation of this amount.

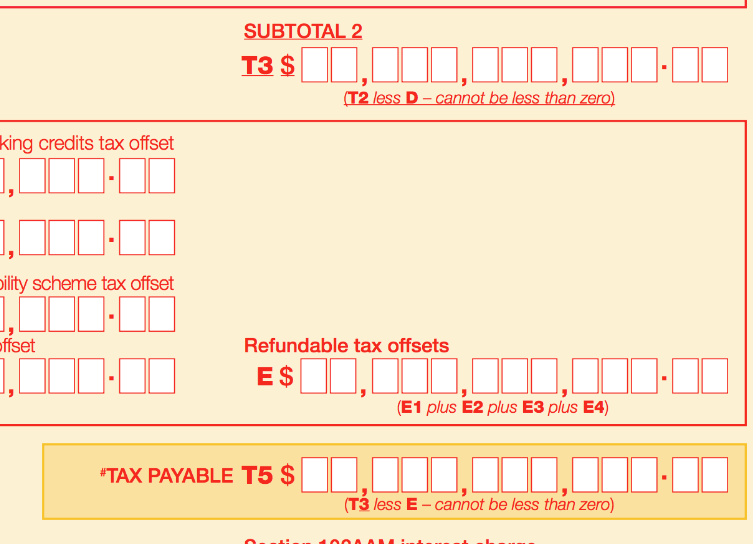

Section D: Income tax calculation statement - Totals

New label (T3) and updated label T5 descriptor at Q13

T3 Subtotal 2

Take D Non-refundable carry forward tax offsets away from T2 Subtotal 1.

If the answer is:

- positive, SF360 will write the answer at T3

- zero or negative, SF360 will write 0 at T3.

If the non-refundable carry forward tax offsets are greater than the subtotal at T2, the excess may be carried forward and applied in a later income year.

T5 Tax payable

Is the amount at T3 Subtotal more than the amount at E Refundable tax offsets?

|

No |

|

|

Yes |

|

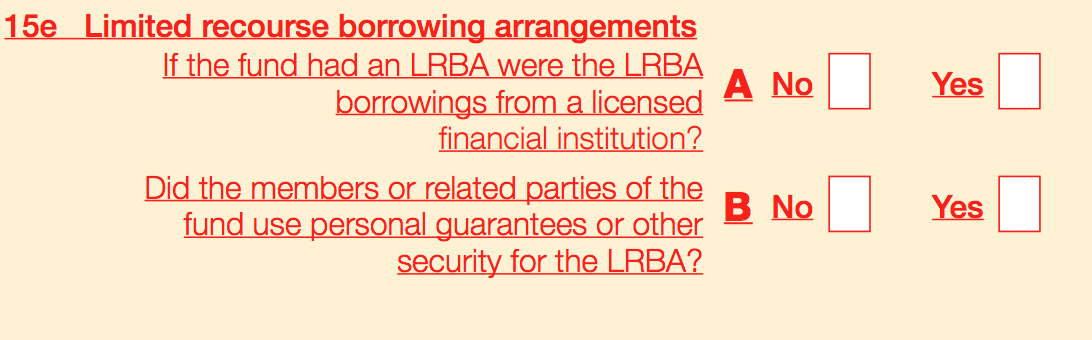

Section H: Limited recourse borrowing arrangements (LRBAs)

New question (Q15e) for statistics

If the fund had an LRBA, were the LRBA borrowings from a licensed financial institution?

A licensed financial institution includes a bank or approved deposit taking institution. Examples of licensed financial institutions include:

- Australian-owned banks

- foreign banks (branches or subsidiaries)

- credit unions

- building societies

- authorised non-operating holding companies

- finance companies.

Answer 'No' if the fund borrowed money under the LRBA from:

- a related party of the fund

- a non-licensed financial institution

Also answer 'No' if the fund holds more than one LRBA, and the money to acquire at least one (or part) of an asset has been borrowed from a source other than a licensed financial institution.

Did members or related parties of the fund use personal guarantees or other security for the LRBA?

Answer 'Yes' if:

- a member of the fund or a related party of the fund has provided a personal guarantee or security for the LRBA

- the fund holds more than one LRBA, and a member or a related party has used a personal guarantee or other security for at least one of the LRBAs.

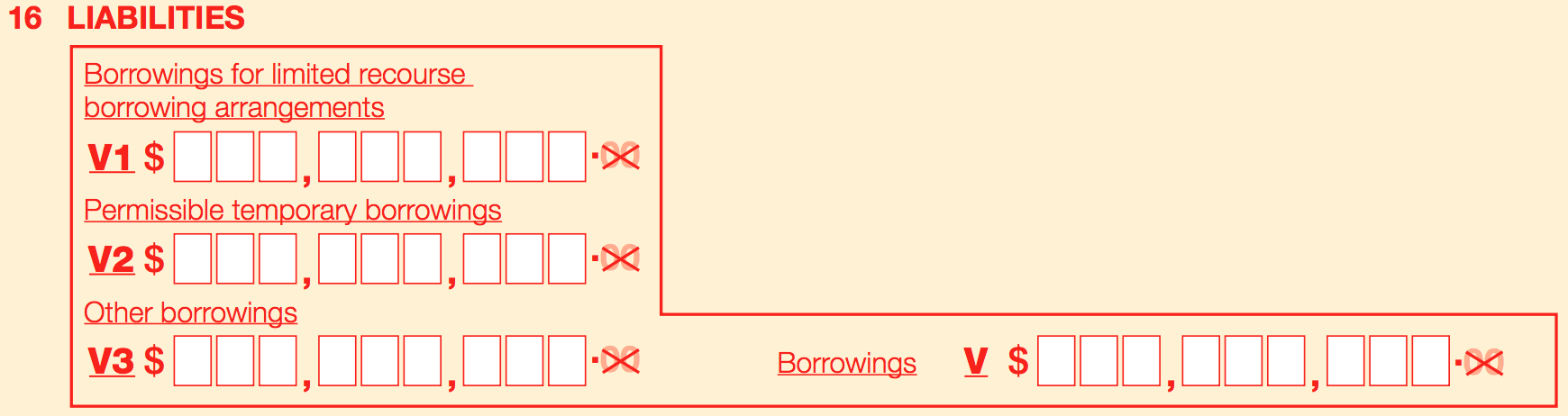

Section H: Liabilities and Borrowings

Following the 2015 Murray Inquiry, there are no LRBA restrictions on SMSFs. However, the ATO monitors the risk and leverage of SMSFs and reports to Government. Consequently, we have added questions about the use of LRBAs and additional borrowings.

You will find three additions to 16 V Borrowings to report LRBAs, temporary borrowings and other borrowings.

Write at V1 to V3 the total value of each type of outstanding borrowing by the SMSF (including accrued interest) on 30 June 2017.

V1 Borrowings for limited recourse borrowing arrangements

- Write at V1 the value of outstanding borrowings held under all limited recourse borrowing arrangements at 30 June 2017.

- Do not include the value of the assets held under the limited recourse borrowing arrangement here.

- The values of the assets held on trust under limited recourse borrowing arrangements are to be included at J1 to J6 and the total at J of iItem 15bB.

- If the SMSF reports borrowings for an LRBA at V1, it must also report at: J Limited recourse borrowing arrangements

V2 Permissible temporary borrowings

Write at V2 the value (on 30 June 2017) of any permissible temporary borrowings held by the SMSF.

Permissible temporary borrowings are those borrowings allowed under subsections 67(2), (2A) and (3) of the Superannuation Industry (Supervision) Act 1993, and include:

- borrowing money for a maximum of 90 days to meet benefit payments due and required to be made to members, or to meet an outstanding superannuation surcharge liability (where, in either case, the SMSF would not able to make such a payment without the borrowing), provided the borrowing does not exceed 10% of the value of the SMSF's total assets

- borrowing money for a maximum of 7 days to cover the settlement of certain security transactions (where, at the time the relevant investment decision was made, it was likely that the borrowing would not be required), provided the borrowing does not exceed 10% of the value of the SMSF's total assets.

V3 Other borrowings

Write at V3 the value (on 30 June 2017) of all other borrowing amounts.

Example: SMSF with multiple borrowings

At 30 June 2017, an SMSF has a beneficial interest in residential land with a market value of $400,000 held under a limited recourse borrowing arrangement.

The outstanding amount borrowed under the limited recourse borrowing arrangement at that time is $150,000.

The SMSF also has $5,000 in permissible temporary borrowings to meet benefit payments due to members.

The SMSF reports:

|

V1 Borrowings for limited recourse borrowing arrangements |

$150,000 |

|

V2 Permissible temporary borrowings |

$5,000 |

|

V3 Other outstanding borrowings |

(Blank) |

|

V Borrowings |

$155,000 |

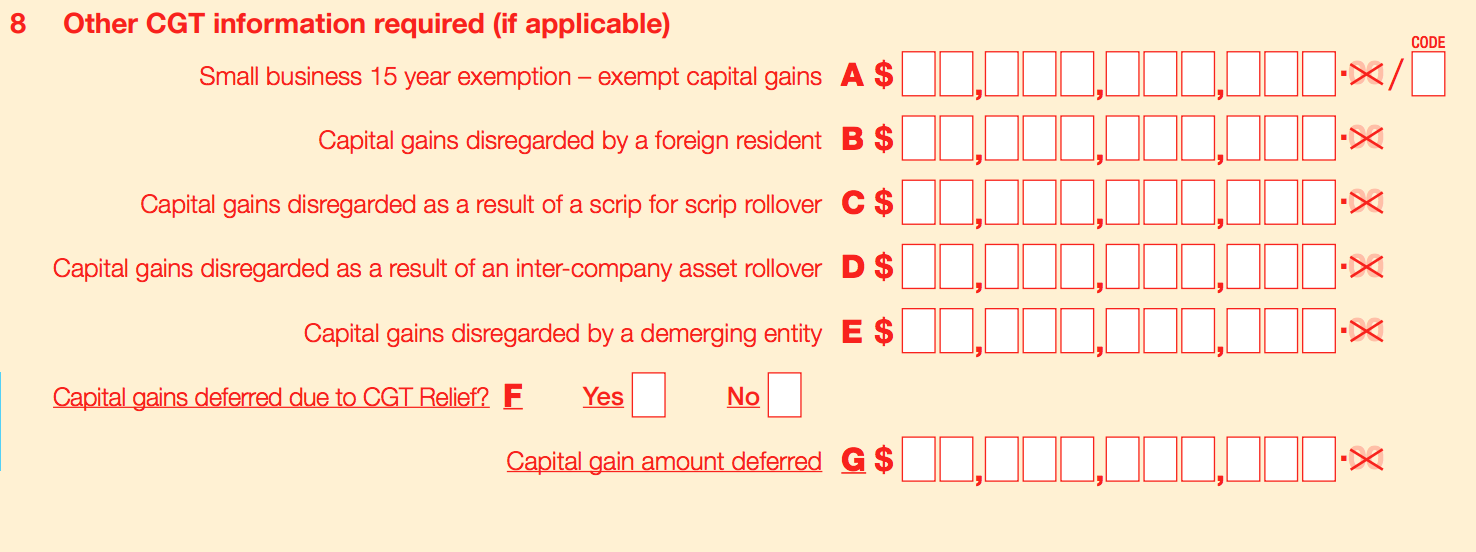

2017 CGT Schedule: CGT Relief

- New labels (F & G) at Q8

- Taxpayer's declaration moved to page 4 as a result of the change above

Transitional CGT Relief

Transitional CGT relief is available for SMSFs to provide temporary relief from certain capital gains that might result from individuals complying with the transfer balance cap, and Transition-to-Retirement Income Stream (TRIS) reforms, which commenced on 1 July 2017. It applies to certain CGT assets held by a complying SMSF at all times between the start of 9 November 2016, to ‘just before’ 1 July 2017.

CGT relief is not automatic. It must be chosen by a trustee for a CGT asset. If CGT relief is chosen, the trustee will need to advise the ATO in the CGT schedule on, or before, the day they are required to lodge their fund’s 2016-17 income tax return. The decision is irrevocable.