Note

BGL do not provide accounting or taxation advice. The following is designed to act as a guide for Simple Fund 360 users. It is not designed to be accounting or tax advice and should not be taken as a strict guideline. Other methods that are more suitable may be used instead of these steps.

Details

Telstra undertook an off-market buy-back of its own shares.

For more detailed information refer to the following documents:

Scenario

In this example, it is assumed that 1,000 TLS shares have been bought back.

The deemed capital proceeds are $2.70 per share which is the capital component ($1.78) plus $0.92 per share (amount by which the CGT value exceeds the Buy-Back price).

The dividend component amounts to $2.65 per share.

Refer to the Buy-Back Consideration Statement from Telstra for these details.

Simple Fund 360 allows multiple transactions occurring on the same day to be posted as one journal entry. A single journal entry will be used to record the transactions. Please note that you can split this into multiple journals if you wish.

| Steps | Details | DR | CR |

|---|---|---|---|

| Step 1 | Record the share buy-back ($2.70 per share) | $2700 | |

|

Record the difference between the deemed capital proceeds ($2.70 per share) and the capital component ($1.78 per share) = $0.92 per share |

$920 | ||

| Step 2 | Enter the Dividend Component ($2.65 per share) | $2650 | |

| Step 3 | Input the Total Bank Receipt | $4430 |

In this example, we are going to use Account 37500/TLS to record the difference ($0.92 per share) between the deemed capital proceeds ($2.70 per share) and the capital component ($1.78 per share). As this is a non-deductible expense, we need to change the tax label of Account 37500/TLS.

If you are already using 37500/TLS to record deductible expenses, you can create a new expense account and change the label by following the steps below.

To change the label, follow the steps below:

- Go to Accounting | Chart of Accounts.

- Search for and select 37500/TLS.

- Select More Details>>.

- Change the Tax Label to Not Applicable - Permanent Difference.

- Select Save.

You can refer to the Non Tax-Deductible Expenses help for more detailed information.

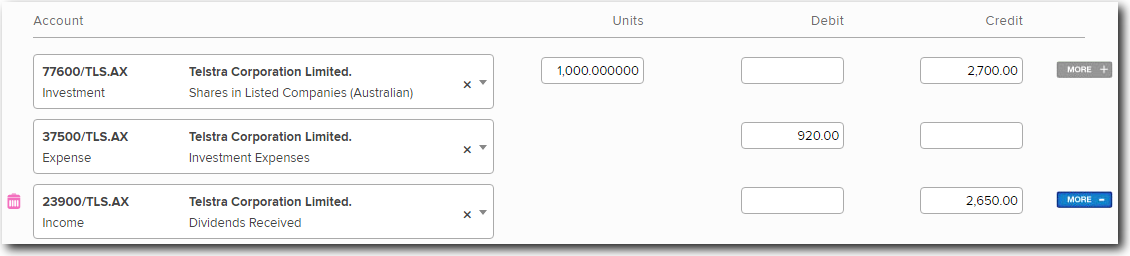

Step 1 - Record the share buy-back and the difference between the deemed capital proceeds and the capital component

- Go to Accounting | Transaction List.

-

Select New Transaction and then Journal from the drop-down list.

-

Input the Receipt Date in the Date Field and a Reference number. You can include a description of the transaction in the Description box.

-

Record a disposal to the 77600/TLS account. The consideration amount is $2.70 x number of shares bought back.

-

Review the Disposal Details panel. You can change the Contract Date if required to match the date the shares were actually bought back. Refer to the Buy-Back Consideration Statement from Telstra for this information.

-

Next, record the difference ($0.92 per share) between the deemed capital proceeds ($2.70 per share) and the capital component ($1.78 per share) as a non-deductible expense. On the next line under the Account heading, click into the Select an account box and locate Account 37500/TLS (the tax label was changed to Not Applicable - Permanent Difference - refer to instructions above).

-

Input the debit amount for the expense ($0.92 x 1000 = $920 in this example).

Step 2 - Record the dividend component

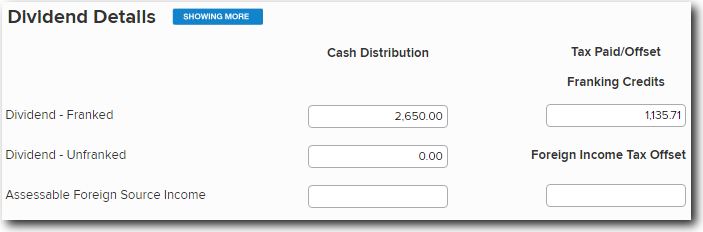

Refer to the Buy-Back Consideration Statement from Telstra to confirm payment details and franked amount.

Dividend amount = $2.65 x number of shares bought back

To record this, select Add line to add a new transaction line. Under the Account heading, search for the Telstra dividend account by typing 23900/TLS in the Select an account box. Input total dividend amount under the Credit column ($2650 in this example) and review the Dividend Details to ensure they are correct.

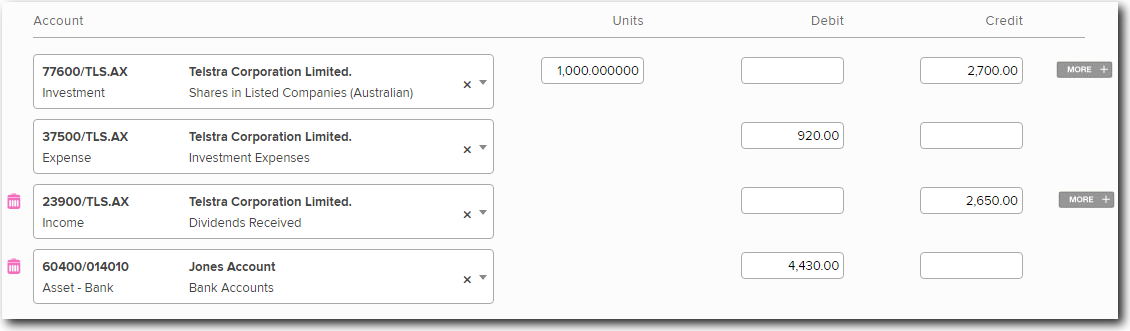

Step 3 - Record the receipt to the bank

-

Select Add line to add a new transaction line. Under the Account heading, search for the Bank account by typing 60400 in the Select an account box and input $4430 under the Debit column.

- Select Post.