Note

BGL do not provide accounting or taxation advice. The following is designed to act as a guide for Simple Fund 360 users. It is not designed to be accounting or tax advice and should not be taken as a strict guideline. Other methods that are more suitable may be used instead of these steps.

Details

Iron Mountain Incorporated (INM) acquired Recall Holdings (REC) through a scheme of arrangement.

The scheme was implemented on 2 May 2016.

All Recall shareholders as of the record date, 27 April 2016, could elect one of the following options:

Option 1 - Standard Consideration

For more information on the scheme, refer to the following:

Option 1 - REC shareholders elected to receive a combination of cash and INM shares/CDIs

The fund held 1000 REC shares as at 27 April 2016. Assuming the fund did not make a valid Cash Election, then it would receive the following (See CR 2016/30 Point 23):

-

INM shares or CDIs - 0.1722 INM share for each Recall share held (CR 2016/30 Point 23)

-

Cash component

Cash Consideration x number of REC shares currently held = $0.6485 x 1000 = $648.50 (CR 2016/30 Point 26)

Instructions

-

Calculate the cost base of REC shares attributable to the cash component.

-

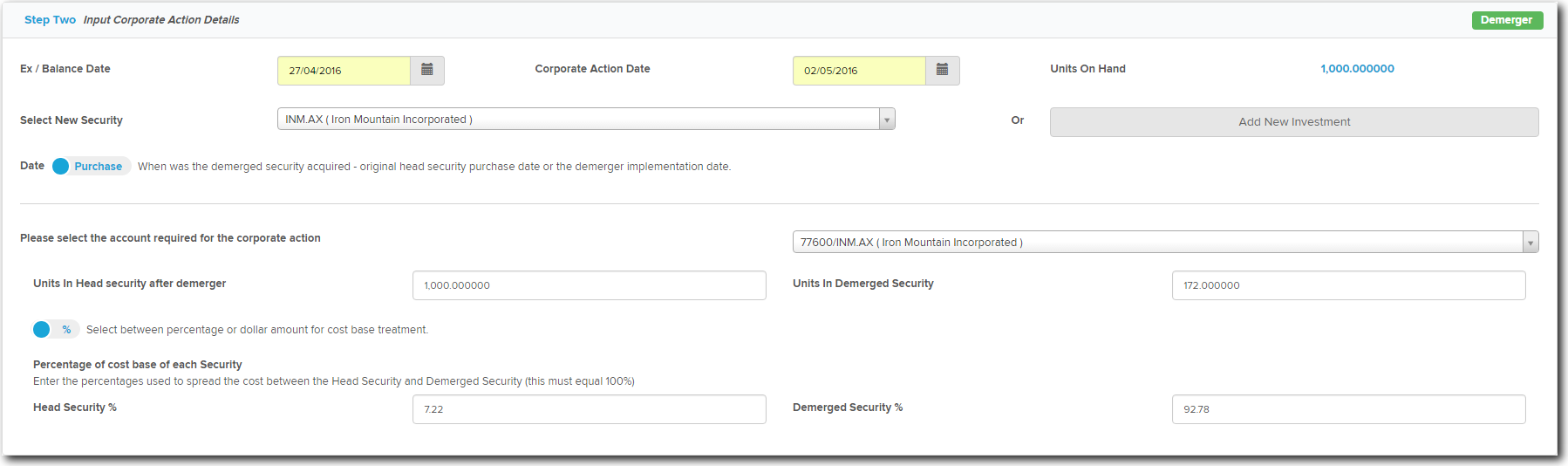

The Capital Component will be recorded using the Demerger function in Simple Fund 360. Go to Investments | Corporate actions and select New Corporate Action.

As the fund has chosen scrip for scrip rollover, the Date has been set to

so that the contract date of the INM shares will be the original purchase date of the REC shares.

so that the contract date of the INM shares will be the original purchase date of the REC shares.Otherwise, change it to

for the contract date of the INM shares to be the Corporate Action date.

for the contract date of the INM shares to be the Corporate Action date. -

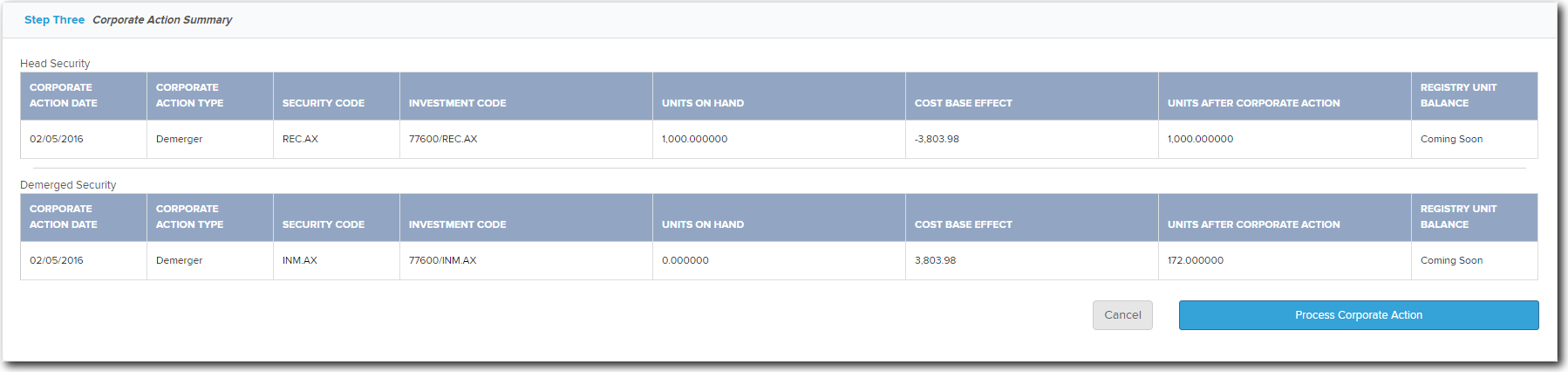

Review the Corporate Action Summary.

-

Select Process Corporate Action.

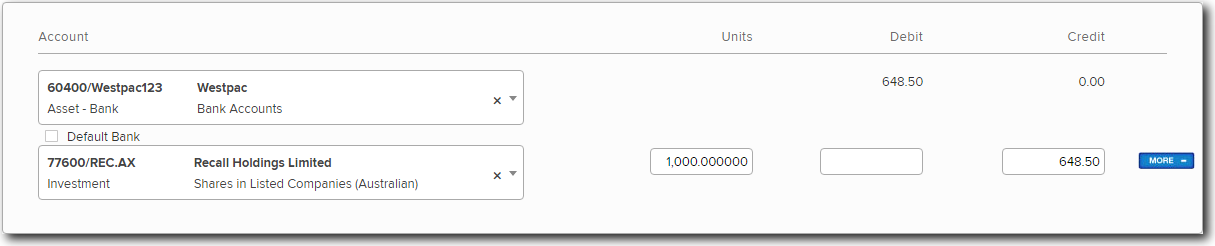

- To record the Cash Component, go to Accounting | Transaction List and add a new Bank Statement transaction.

- Simple Fund 360 will calculate the capital gains. Capital gains that are referable to the receipt of cash cannot be the subject of a roll-over. (See CR 2016/30 Point 26)

- Select Post to save the transactions.

Option 2 - Recall shares are exchanged for cash consideration

You will need to dispose of the REC shares.

In this example, it is assumed that there is no scale back and the consideration received per share is $8.50. (CR 2016/30 Point 23)

Please check the statement from Recall for the actual consideration amount received.

Go to Accounting and select Bank Statement under Add New Transaction.

Enter the disposal details.

Select Post to save the transaction.