What has changed?

For the 2017–18 to 2020–21 income years, you will need to consider if the SMSF holds disregarded small fund assets. If it does, you must use the proportionate method to calculate Exempt Current Pension Income (ECPI).

From the 2021–22 income year onwards there are two changes for SMSFs when claiming ECPI:

- If an SMSF is in 100% retirement phase at all times of the year, the disregarded small assets rule does not apply, and the fund's assets are segregated current pension assets.

-

The fund may choose to use either the segregated method or the proportionate method to calculate ECPI for the income year when:

- an SMSF is paying a retirement-phase income stream

- the fund isn't 100% in retirement phase (for example, if some assets are supporting accumulation interests); and

- the fund doesn't have disregarded small fund assets.

Changes to Simple Fund 360

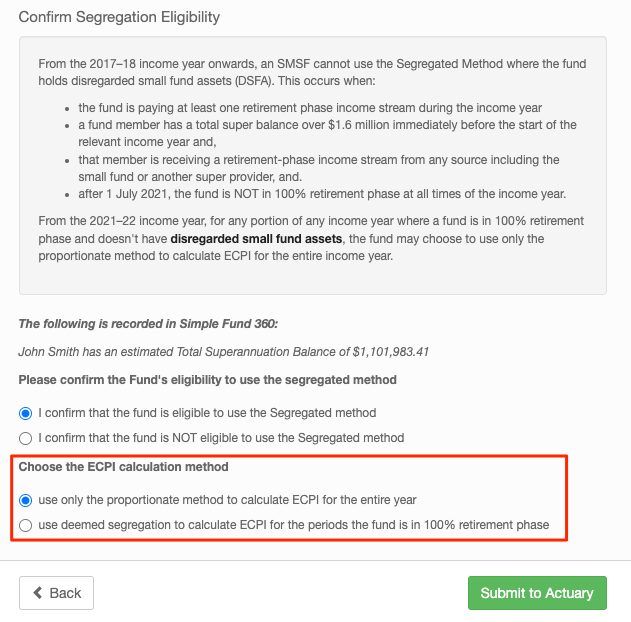

A new question will display for the 2022 and later Financial Years in the Actuarial Certificate Wizard.

- The question will only display where “The fund is eligible to use the segregated method” is selected

- The response to this question will be sent through to your select Actuary.

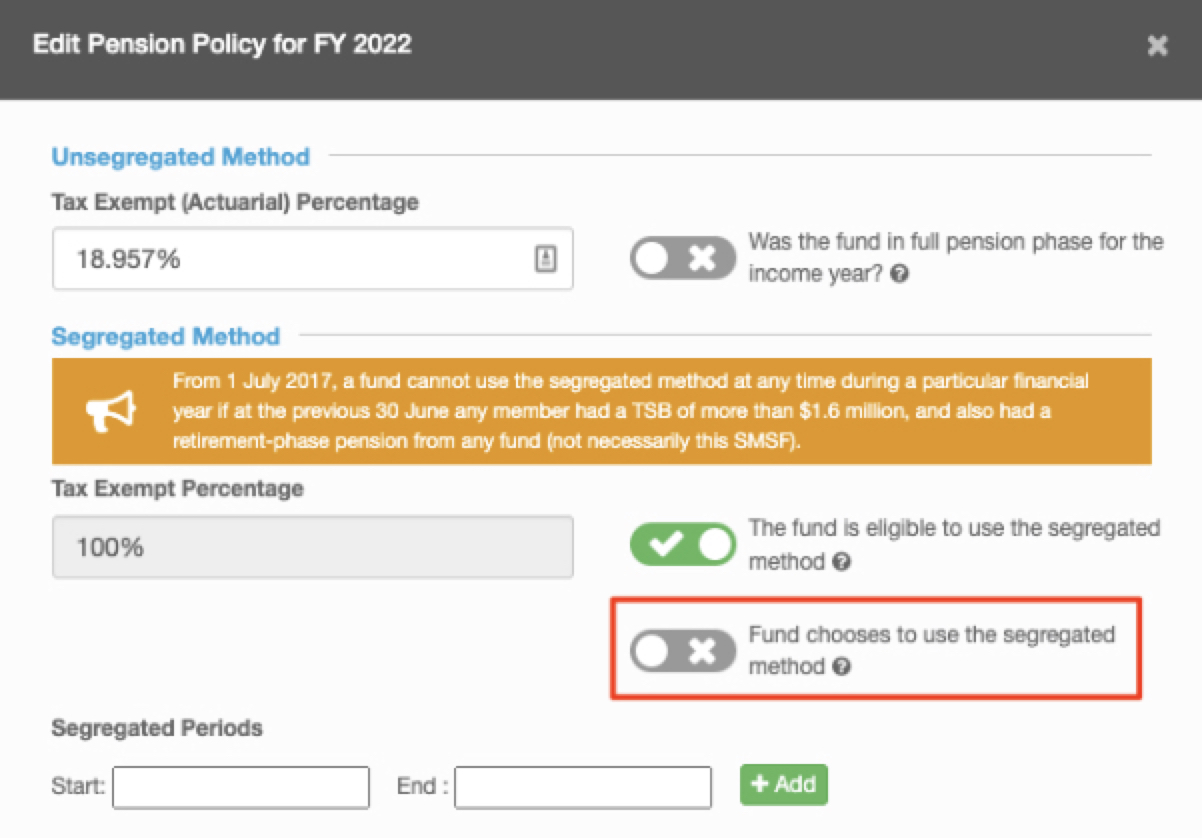

Users can manually edit or insert this into the Pension Policy as well.

Resources

- ATO - Methods for calculating ECPI

- DBA Lawyers - New choice simplifies ECPI claims via the unsegregated or actuarial method

- Podcast - Navigating the latest ECPI changes with SMSF clients