Rio Tinto has successfully completed its off-market buy-back, achieving its share purchase target of approximately 41.2 million Rio Tinto Limited shares, for a total consideration of A$2,871 million (US$2,081 million).

The key features of the Buy-Back are as follows:

|

Value of Shares bought back |

A$2,871,097,958 |

|

Market Price |

A$81.0268 |

|

Buy-Back Discount |

14% |

|

Ex-entitlement to participate in the Buy-Back |

25 Sept 2018 |

|

Record date |

26 Sept 2018 |

|

Buy-Back payment date |

19 Nov 2018 |

|

Buy-Back Price |

A$69.69 |

|

Capital component per Share |

A$9.44 |

|

Fully franked dividend component |

A$60.25 |

|

Tax Value |

A$77.80 |

|

Number of Shares bought back |

41,198,134 |

|

Percentage of Rio Tinto Limited issued shares bought back |

9.99% |

|

Scale back |

58.27% |

For Australian capital gains tax purposes, the deemed capital proceeds are expected to be A$17.55, being the A$9.44 capital component plus A$8.11, which is the amount by which the Tax Value exceeds the Buy-Back Price.

How to process in Simple Fund 360

Example:

Fund has 1,000 units in RIO.AX participating in the buy-back, with a cost base of $5,000.

Deemed Capital Proceeds = $17.55 x 1,000 units = $17,550

Franked Dividend Component = $60.25 x 1,000 units = $60,250

Excess Tax Value over Buy-Back Price = $8.11 x 1,000 units = $8,110

Buy-Back Proceeds = $69.69 x 1,000 units = $69,690

SF 360 allows multiple transactions occurring on the same day to be posted as one journal entry. As all of the following transactions happened on the same date, a single journal entry will be used to record them. Please note that you can split this into multiple journals if you wish.

Step 1: Record the capital proceeds

- Go to Accounting | Transaction List.

- Select New Transaction and then Journal from the drop down list.

- Enter the Payment Date as 19/11/2018, reference and description. Refer to the buy-back payment and dividend statement received from Rio Tinto for more details.

- Record a disposal to the RIO.AX investment account with deemed capital proceeds of $17,550.

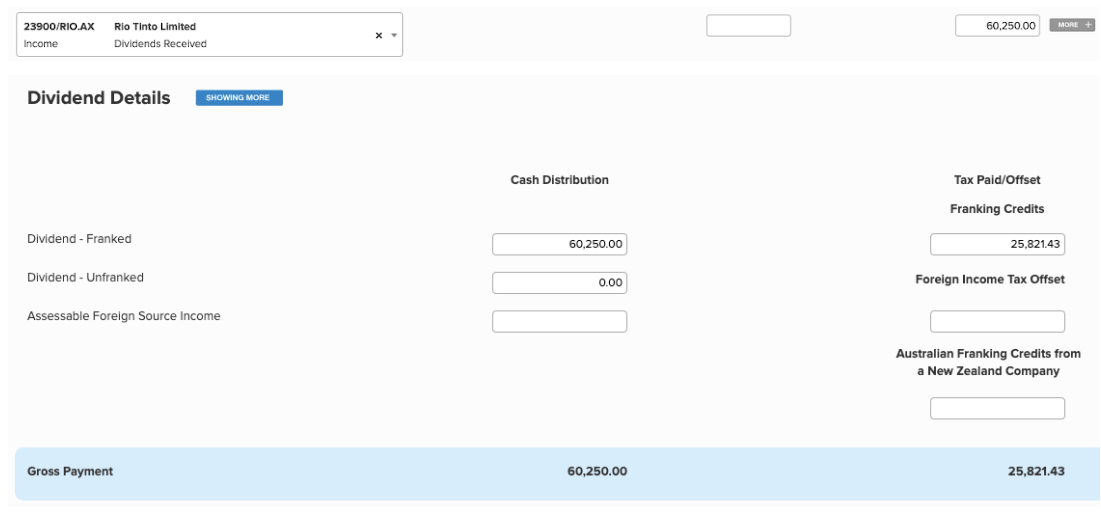

Step 2: Record the dividend component

- Record dividend amount of $60,250 to the linked dividend account under Credit column. Franked Dividend and Franking Credits would be automatically populated in the dividend details.

Step 3: Record the excess tax value over buy-back price

- The excess tax value over buy-back price ($8.11 per share) i.e. difference between the deemed capital proceeds ($17.55 per share) and the capital component ($9.44 per share) needs to be recorded as a non-deductible expense.

- The non-deductible expense account needs to have the tax label setup as follows.

- Go to Accounting | Chart of Accounts.

- Search for the linked expense account you are using. In this example we are using 37501/RIO.AX.

- Change the Tax Label to Not Applicable - Permanent Difference.

- Select Save.

You can refer to the Non Tax-Deductible Expenses help for more detailed information.

Enter the excess tax value amount of $8,110.

Step 4: Record the receipt to the bank

- Record buy-back proceeds of $69,690 to the bank account.

- Post the transaction.

All transactions once recorded:

.