Overview

This article will walk you through recording common events that occur over the entire ownership period of a rental property, which applies to SMSFs and Non-SMSF entities.

The events looked at include:

- Purchase of property including deposit and settlement of property.

- Improvements to the property.

- Acquisition of depreciable assets in the property.

- Capital works deductions.

- How to record rental property income and expenses.

- Disposal of depreciable assets in the property.

- Disposal of the rental property.

Example

Note: This example is adapted from the following ATO example found here: Selling a rental property

The fund bought a residential rental property for a purchase price of $750,000. The property was subject to an LRBA and financed through a $200,000 loan.

In addition to the purchase price, the fund paid stamp duty and legal fees of $30,000.

After purchase the fund improved the property by constructing a fence for $6,000.

Over the three years of ownership of the property, the fund claimed $25,000 in depreciation expenses for assets within the rental property. The fund also claimed $35,000 in capital works deductions.

In November 2017 the fund sold the property for $900,000. The cost of sale incurred by the fund was $10,000.

The fund would attract the following capital gain on sale.

| Capital Gain | 164,000 | |

| Item | Amount($) | Total ($) |

| Proceeds | 900,000 | 900,000 |

| Purchase amount | 750,000 | |

| Stamp duty and legal fees | 30,000 | |

| Fence | 6,000 | |

| Depreciation on assets | (25,000) | |

| Capital works deductions | (35,000) | |

| Disposal costs | 10,000 | |

| less Cost base | (736,000) |

Purchase of property and cost base adjustments

There are many ways to record the purchase and settlement of a property, the journal below is shown as an example.

For items that need to be capitalised, such as Stamp Duty, Legal Fees, etc., users can record a cost base adjustment to the property purchase. Also, refer to How to Enter an Investment Cost Base Adjustment for more information.

Deposit for property:

| Account Name | Account Code | Units | DR ($) | CR ($) |

| Investment Property | 77200/Property | 1 | 50,000 | |

| Bank | 60400/Bank | N/A | 50,000 |

Settlement of Property including stamp duty and legal fees:

| Account Name | Account Code | Units | DR ($) | CR ($) |

| Investment Property | 77200/Property | 0 | 730,000 | |

| Bank | 60400/Bank | N/A | 530,000 | |

|

LRBA Loan Account (or Investment Loan for Non-SMSF entities) |

85500/Property (or 85660/Property for Non-SMSF entities) |

N/A | 200,000 |

Addition of fence to property:

| Account Name | Account Code | Units | DR ($) | CR ($) |

| Investment Property | 77200/Property | 0 | 6,000 | |

| Bank | 60400/Bank | N/A | 6,000 |

For this example, the addition of the fence will be treated as a cost base adjustment.

Note

When recording a cost base adjustment to an existing property, enter Units as "0" instead of "1". Otherwise, the units will be doubled up, resulting in unintended consequences.

Also refer to the following articles:

Rental Property Liabilities

Upon the creation of a property account, the program will automatically create a linked account 83000 (Investment Liabilities). Alternatively, you can create a new account in the 80000 range and link it back to the property. See these pages for more:

- Chart of Accounts

- Linked Accounts

- Limited Recourse Borrowing Arrangements (LRBA) - for loan liabilities

- Adding a Loan Account - Investment Loans for Non-SMSF entities

Depreciable Assets

Acquisition

The entity has two options in choosing how to process the acquisition of the investment property's depreciable assets.

Which option to use will depend on whether:

- The depreciable asset was part of the property when it was purchased; or

- The depreciable asset was added to the property after the property's purchase

The following journals would be used to record each scenario:

The depreciable asset was part of the property when it was purchased:

| Account Name | Account Code | Units | DR ($) | CR ($) |

| Depreciable Asset | 72650/DepAsset | 1 | XX,XXX | |

| Investment Property | 77200/Property | 0 | XX,XXX |

The depreciable asset was added to the property after the property's purchase:

| Account Name | Account Code | Units | DR ($) | CR ($) |

| Depreciable Asset | 72650/DepAsset | 1 | XX,XXX | |

| Bank | 60400/Bank | N/A | XX,XXX |

Depreciation

The entity will use the depreciation schedule to depreciate the assets that came with the property when it was purchased.

For more information on posting depreciation amounts, please refer to: How to Enter Depreciation

Capital Works Deductions

Record the Capital Works Deductions as a tax adjustment for each financial year.

Alternatively, users can process Capital Works Deductions using the Depreciation Schedule by selecting the Capital Works Deduction depreciation method.

Please note that when capital works adjustments are recorded, Simple Fund and Simple Invest 360 will automatically reduce the cost base by the recorded capital works adjustments on the investment's disposal. There is no need to perform any additional journals to write back the recorded capital works adjustments.

The capital gain calculated can be confirmed by viewing the CGT Register Report.

Rental Income and Expenses

Multiple rental property income and expenses for the one property can be recorded using a single transaction. Simple Fund and Simple Invest 360 provides a Rental Details panel which records a running balance of the rental property transactions as they are input. This panel also provides an income and expense report for the financial year to date.

| From the Main Toolbar, select Accounting |  |

| Select Transaction List |  |

1. From the Transaction List screen, select New Transaction. From the drop-down list, select Bank Statement.

2. Input the date of the transaction and a reference number (Simple Fund 360 will automatically produce a reference number, but it is editable). You can include a description of the transaction in the Description box.

3. Under the Account heading, select the bank account from the Select an account box.

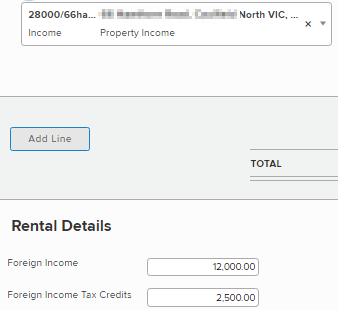

Record the Rental Property Income

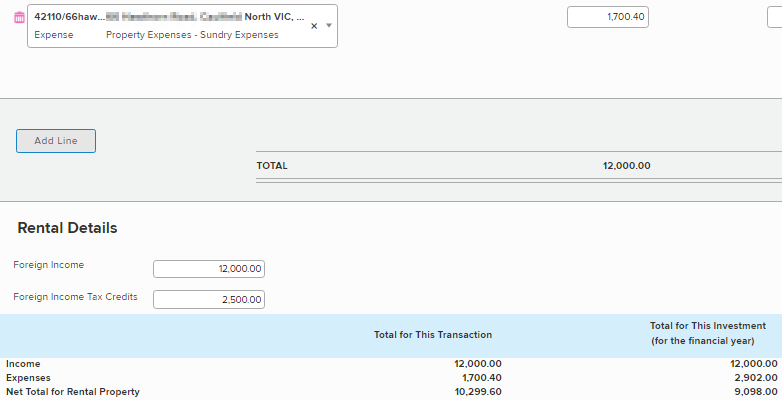

Begin typing and select account 28000/INVESTCODE from the Select an account box. Input the rental income amount received. If the rental income is from a foreign source, record the income and Foreign Tax Credits in an additional field as well. (The foreign sourced rental income will display at label D1 in the SMSF Annual Tax Return)

Record the Rental Property Expenses

To record expenses to the same transaction select Add Line for each additional transaction. Begin typing and select the rental property expense (account range 41910/INVESTCODE to 42120/INVESTCODE) from the Select an account box.

Input the rental expense amount paid (for each expense). The program will post a corresponding entry to the bank account fields on the screen (if you post a Debit amount to the other account, the program will post a Credit to the bank for the same amount, and vice versa).

Simple Fund and Simple Invest 360 will record the income and expenses in the Rental Details panel which will appear below. This will provide you with a NET total of the property's activity.

Rental Property Statements

Simple Fund 360 allows you to produce a Rental Property Statement detailing the income and expense transactions for an investment property. Refer to the Rental Property Statements help for further information.

Selling the property

Disposal of depreciable assets

When selling the property, the depreciable assets will need to be disposed of at their written down value first. The written-down value for the depreciable asset will need to be calculated until the disposal date.

Ensure that the Asset subject to CGT box is unticked for the depreciable asset in the More Details section for the account.

The following journal will be used to dispose of the depreciable assets and adjust the cost base of the property:

| Account Name | Account Code | Units | DR ($) | CR ($) |

| Investment Property | 77200/Property | 0 | WDV | |

| Depreciable Asset | 72650/DepAsset | 1 | WDV |

WDV = Written down value of asset up until disposal date

Cost of sale

The costs of sale incurred in selling the property will be added to the cost base of the property. This will be recorded as a cost base adjustment:

| Account Name | Account Code | Units | DR ($) | CR ($) |

| Investment Property | 77200/Property | 0 | 10,000 | |

| Bank | 60400/Bank | N/A | 10,000 |

Disposal of property

The disposal of the property will be recorded by recording the proceeds from the sale.

| Account Name | Account Code | Units | DR ($) | CR ($) |

| Bank | 60400/Bank | N/A | 900,000 | |

| Investment Property | 77200/Property | 1 | 900,000 |

In the CGT Register Report, the calculated Gross Discounted Gain can be seen as $164,000.