Note

BGL do not provide accounting or taxation advice. The following is designed to act as a guide for Simple Fund 360 users. It is not designed to be accounting or tax advice and should not be taken as a strict guideline. Other methods that are more suitable may be used instead of these steps.

Details

Under the Entitlement Offer, eligible NAB shareholders are entitled to acquire 2 new shares for every 25 existing fully paid ordinary shares held on Tuesday 12 May 2015 at 7:00pm (Entitlement)

The way you process this offer in Simple Fund 360 will depend on which option the trustees of the fund have chosen.

| Option | If the trustees: | You will need to: |

|---|---|---|

| 1 | Exercised their Entitlement |

Enter a purchase Transaction for the new shares at the discounted price. See Option 1. |

| 2 | Sold their Entitlement through ASX |

Enter a purchase for the ASX code: NABR with a cost base of $0 and sell the Entitlement for the amount received. See Option 2. |

| 3 | Did not exercise or sell their Entitlement and received a premium at the end of the process |

Option A: Treated as a Capital Gains Enter a purchase for the ASX code: NABR with a cost base of $0 and sell the Entitlement for the amount received. See Option 3. Option B: Treated as Unfranked Dividend or Other Income If the tax treatment in TR 2012/1 should be applied, record the premium as either an unfranked dividend or other income. See Option 3. |

| 4 | Did not exercise or sell their Entitlement and did not receive a premium at the end of the process | No transactions are required. |

For more information, refer to the following documentation:

Example

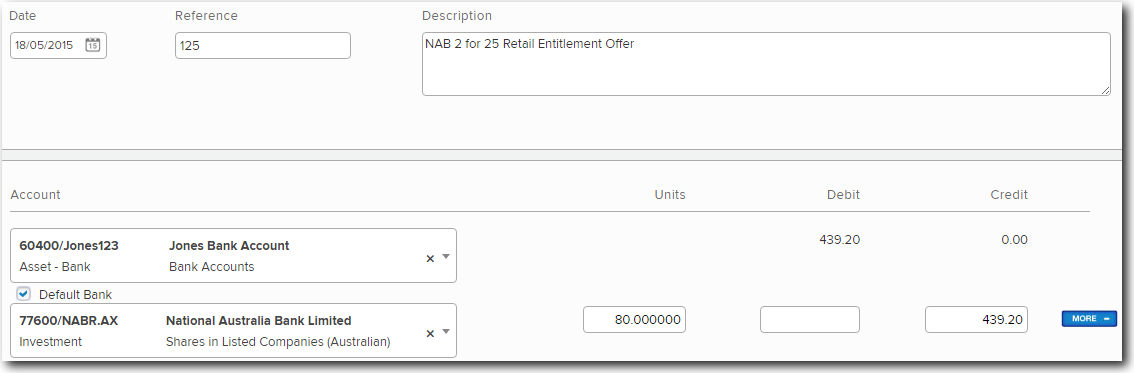

The fund held 1000 NAB shares as at 12 May 2015.

The number of shares the fund is entitled to is 80 (1000/25 x 2).

The offer price is $28.50 as per the Retail Entitlement Booklet.

The premium received per entitlement is $3.10. See NAB ASX Announcement - Retail Shortfall Bookbuild.

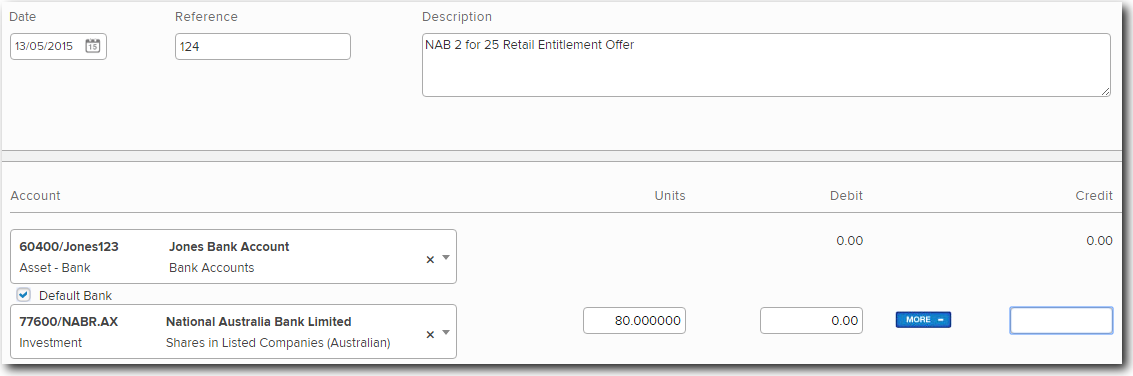

The trustees have exercised the Entitlement

In this scenario, the fund held 1000 NAB shares as at 12 May 2015.

Therefore, the fund is entitled to 80 new shares (1000/25 x 2).

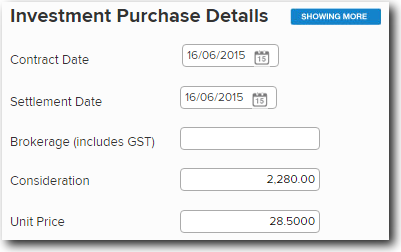

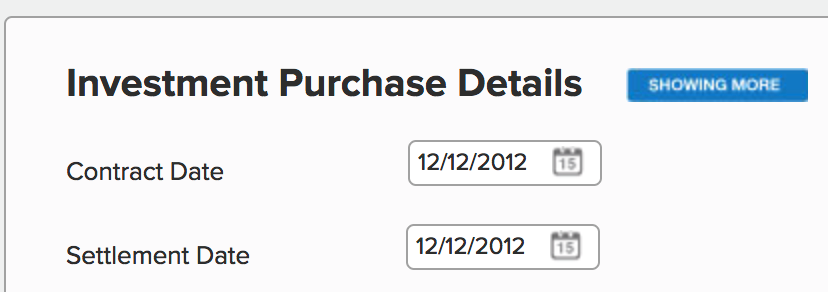

Go to Accounting | Transaction List and process a purchase transaction for the new 77600/NAB shares at the discounted price.

If the settlement date is different to the contract date, you can change the dates by selecting More to access the Investment Purchase Details.

In this example, the transaction details are based on the information provided in the Retail Offer Booklet. Refer to the statement you have received from NAB for more details about the date, units and price.

The trustees have sold the Entitlement

- Go to Accounting | Transaction List and process a purchase for the ASX Code:NABR with a cost base of $0.

Note: The Contract Date should be changed to the Original Parcel date for CGT Discount to apply.

- From the Transaction List screen, process a disposal to sell the entitlements for the amount received. Simple Fund 360 will calculate the proceeds as capital gains as per specified in the NAB advice.

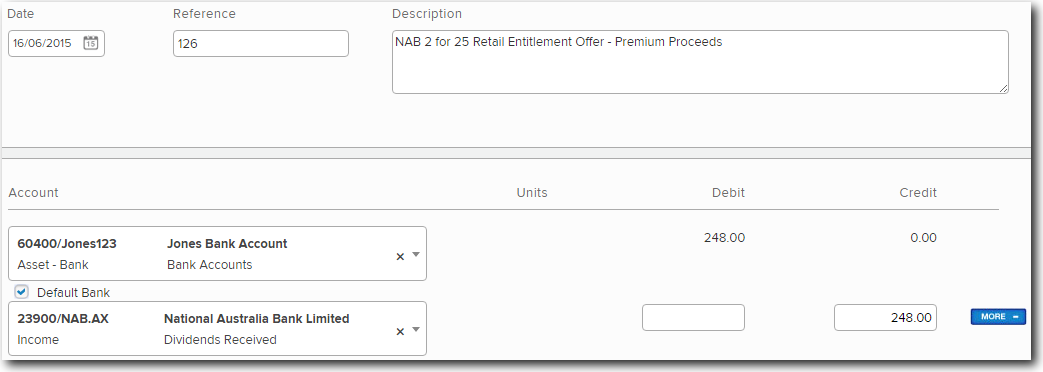

The trustees did not exercise or sell their Entitlement and received a premium

There are two possible ways to record this:

- Option A - Treated as Capital Gains

- Option B - Treated as Unfranked Dividend or Other Income

Option A - Treated as Capital Gain

The recommendation by NAB's tax advisers is that any premium should be treated as a capital gain and that ATO Taxation Ruling 2012/1 does not apply as the Entitlements are tradeable on ASX.

- Process a purchase of the Entitlements with a cost base of $0. Note:The Contract Date should changed to the Original Parcel date for CGT Discount to apply.

2. Sell the rights for the amount received

The transactions will be similar to Option 2.

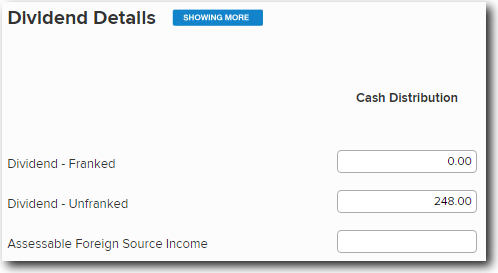

Option B - Treated as Unfranked Dividend or Other Income

If the tax treatment in ATO Taxation Ruling 2012/1 should be applied, you can record the premium as either an unfranked dividend or other income.

For example,