Support Query

How do I process a manual rights issue in Simple Fund 360?

Refer to Share Rights (Notifications) for the Corporate Actions feature to process Rights based on fund investment holdings.

Solution

How to process a rights issue is dependent on the scenario, whether the rights are renounceable or non-renounceable and the course of action undertaken by the SMSF.

Renounceable rights generally offer the SMSF three options on what to do with the rights. They can act on the rights, sell the rights on market or let the rights lapse. There is a potential that the course of action undertaken by the SMSF may result in the processing of more than one of the scenarios below. Renounceable rights are in contrast to non-renounceable rights, which cannot be sold on market or transferred, so scenario 2 below will not apply.

Scenario 1: SMSF Exercises the Rights and takes up the Shares;

Scenario 2: SMSF Sells the Rights on the Market;

Scenario 3: The Rights lapse.

Note

BGL do not provide accounting or taxation advice. The following is designed to act as a guide for Simple Fund 360 users. It is not designed to be accounting or tax advice and should not be taken as a strict guideline. Other methods that are more suitable may be used instead of these steps.

SMSF Exercises the Rights and takes up the Shares

The receipt of rights at nil cost and subsequent purchase of shares is broken down into steps using NAB Rights (NABR.AX) as the example.

Purchase of NAB Rights Issue at cost

- From the Main Toolbar, select Accounting | Transaction List.

- From the Transaction List screen, select New Transaction. From the drop down list, select Bank Statement.

- Input the date of the rights issue to the SMSF and a reference number (Simple Fund 360 will automatically produce a reference number, but it is editable). You can include a description of the transaction in the Description box.

-

Under the Account heading, select the bank account from the Input Bank Account box. Next, select the drop down arrow from the Input Account box below and select Add New Account and select Investment.

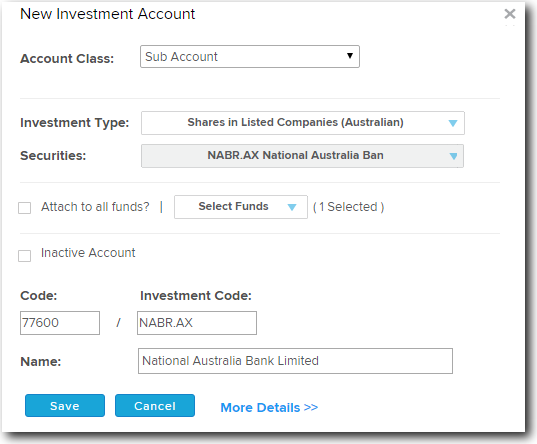

- Add an investment account for the NAB Rights under account code 77600/NABR.AX. Select Save.

- Complete a purchase for the Rights Issue, just like you would an ordinary share purchase (record units). See How to Enter Investment Purchases.

When the Rights are exercised

Two steps are required when the rights are exercised, the disposal of the NABR.AX Rights and subsequent purchase of NAB (NAB.AX) shares.

- Record an Investment Disposal of the NABR.AX rights for $0 consideration.

- Record a Share Purchase on the date of exercise for NAB (security code NAB.AX) shares.

SMSF Sells the Rights on the Market

The receipt of Rights at cost and subsequent disposal of the rights on the market is taxed under the CGT provisions. This example will use NAB Rights (NABR.AX).

Purchase of NAB Rights Issue at cost

- From the Main Toolbar, select Accounting | Transaction List.

- From the Transaction List screen, select New Transaction. From the drop down list, select Bank Statement.

- Input the date of the rights issue to the SMSF and a reference number (Simple Fund 360 will automatically produce a reference number, but it is editable). You can include a description of the transaction in the Description box.

-

Under the Account heading, select the bank account from the Select an account box. Click on the next Select an account box. Select Add New Account and select Investment.

- Add an investment account for the NAB Rights under account code 77600/NABR.AX. Select Save.

- Complete a purchase for the Rights Issue, just like you would an ordinary share purchase (record units). See How to Enter Investment Purchases.

Disposal of the Rights

Complete an investment disposal to account for the consideration and CGT. See Investment Disposal for steps.

The Rights Lapse

If the offer is not taken up, the fund may receive a Retail Premium for the lapse of the rights offer. Depending on the circumstances outlined in the offer document the premium may be treated under the CGT provisions (see scenario 2 above) or as other income (unfranked dividend or other assessable income). If the latter option is used, with reference to the ATO - Taxing Retail Premiums, the income can be processed as an unfranked dividend (account 23900/INVESTCODE) or other investment income (account 26500/INVESTCODE).

- For unfranked dividends, see How to Enter Dividends;

- For other investment income, see Linked Accounts (to add the income account) and Transaction Input.